Understanding the Landscape of Payday Loan Bans Across the United States

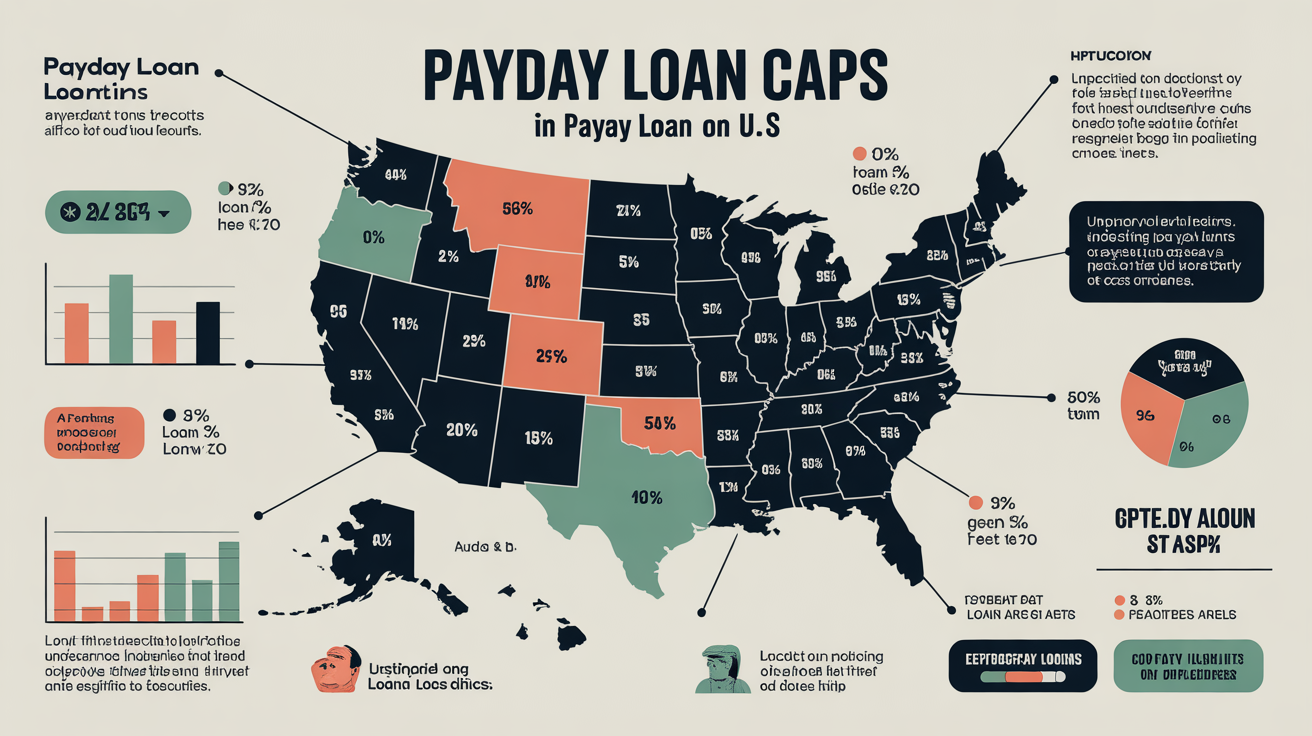

The regulatory environment surrounding payday loan bans by state showcases a diverse array of approaches to consumer protection and financial oversight throughout the United States. Currently, numerous states have enacted stringent measures to either entirely prohibit payday lending or to impose strict limitations on its practice. These legislative actions are designed to defend consumers from exorbitant interest rates and the dangerous cycles of debt that frequently accompany short-term borrowing. On the other hand, some states maintain partial bans, permitting payday loans under certain conditions, while others adopt a more relaxed regulatory stance, allowing payday lending with minimal oversight and restrictions.

States Leading the Charge with Complete Payday Loan Bans

In recent years, a significant number of states have taken bold steps to implement complete bans on payday lending, demonstrating their commitment to safeguarding consumer welfare. States such as California, New York, and New Jersey have successfully outlawed payday loans, citing the necessity of protecting vulnerable populations from the detrimental effects of high-interest borrowing. These complete bans have emerged in response to alarming statistics indicating that payday loans often lead borrowers into prolonged periods of financial distress, with interest rates soaring above 400 percent, trapping individuals in a cycle of debt that is difficult to escape.

The underlying motivation for these sweeping bans stems from a recognition that payday lending often targets individuals in desperate financial situations. Advocates for this type of legislation argue that the elimination of payday loans acts as a crucial protective mechanism for consumers. In states like Massachusetts and Washington, lawmakers have established comprehensive laws that completely prohibit these loans, steering consumers towards more sustainable financial alternatives. The initiatives in these states reflect a broader trend toward prioritizing long-term financial health over the temporary allure of quick cash solutions.

Moreover, these complete bans have ignited discussions regarding the necessity of alternative financial solutions. States that have implemented bans frequently promote community lending initiatives and credit unions, aiming to provide accessible credit options that do not carry the same perilous financial risks as payday loans. This strategy not only protects consumers but also nurtures a healthier financial ecosystem, allowing individuals to secure essential funds without falling victim to predatory lending practices that can lead to insurmountable debt.

Examining States with Partial Bans on Payday Lending

While many states have opted for outright bans on payday lending, others have chosen a more moderate approach, instituting partial bans that impose significant regulations on the payday lending industry. States such as Texas and Illinois exemplify this strategy, allowing payday loans under specific conditions aimed at reducing risks for borrowers. For example, these states might impose interest rate caps, limit the number of loans a consumer can obtain simultaneously, or mandate repayment plans that help prevent borrowers from entering into endless cycles of debt.

The rationale behind these partial bans acknowledges that, while payday loans can be harmful, some consumers may still require access to short-term credit during emergencies. By regulating the industry instead of abolishing it altogether, states like Ohio and Florida strive to strike a balance between consumer protection and the need for immediate financial solutions. These regulations often include mandatory disclosures regarding loan terms and interest rates, equipping consumers with the information they need to make informed financial decisions.

However, the effectiveness of these partial bans remains a topic of ongoing debate. Critics contend that even regulated payday loans can lead to financial instability for borrowers, particularly for those who lack financial literacy. Advocacy organizations have called for more robust measures, advocating for a complete ban to eliminate the risks associated with high-interest borrowing entirely. As these discussions progress, the landscape of payday loan bans by state continues to evolve, reflecting a dynamic interplay between consumer needs and legislative initiatives.

States Maintaining No Restrictions on Payday Lending

Despite the growing trend toward regulation and outright bans, several states still permit payday lending with little to no restrictions. States like North Dakota, South Dakota, and Missouri exemplify this permissive approach, where payday loans are readily accessible. In these regions, payday lenders operate with minimal oversight, and interest rates can skyrocket, often exceeding 400 percent. The absence of bans in these states raises critical concerns regarding consumer protection and the long-term implications for individuals who rely on such financial products.

In states with no restrictions, the payday lending industry continues to flourish, often presenting itself as a viable option for individuals facing urgent financial needs. Advocates for this type of lending argue that the availability of payday loans provides essential credit access, particularly for individuals who may not qualify for traditional loans due to poor credit histories. However, this accessibility comes with a hefty price tag, as many borrowers find themselves ensnared in cycles of debt that lead to further financial difficulties and distress.

Furthermore, states maintaining a permissive approach are increasingly facing pressure from advocacy groups pushing for reform. These organizations emphasize the detrimental effects of payday loans on consumer debt levels and overall financial well-being. As awareness of these issues grows, there is a palpable push for legislative change, with some states reconsidering their stance on payday lending. The ongoing discourse surrounding payday loan bans by state is likely to influence future regulations, as consumer advocates and policymakers strive to find a balance between access to credit and the protection of vulnerable populations.

Tracing the Legislative History of Payday Loan Bans

Grasping the legislative history surrounding payday loan bans by state is critical to understanding the current status and ongoing debates about this contentious financial product. The evolution of payday loan regulations in the United States reveals a complex interplay of consumer advocacy, political will, and economic realities. The journey began in the early 2000s as concerns over predatory lending practices surfaced, prompting lawmakers to take action to protect consumers.

Initial Efforts Toward Regulation

The early 2000s marked a pivotal period in the battle against predatory lending, as various states began to explore regulatory options to manage the rapidly growing payday loan industry. Fueled by alarming narratives of consumers falling into crippling debt, legislators recognized the urgent need for more stringent oversight. During this period, states such as North Carolina and Georgia made early attempts to regulate payday lending by capping interest rates and imposing restrictions on loan amounts.

These initial efforts faced staunch opposition from the payday lending industry, which contended that regulation would restrict access to credit for consumers in need. Despite the pushback, advocacy groups rallied for reform, highlighting the long-term consequences of high-interest loans on vulnerable populations. The dialogue surrounding payday lending began to shift, as more lawmakers contemplated the implications of allowing such financial practices to proliferate unchecked.

As public awareness of predatory lending grew, sentiment increasingly favored stronger regulations. States that enacted initial reforms laid the groundwork for future legislation, demonstrating the potential for meaningful change. This period of early regulation set the stage for comprehensive approaches to payday loan bans, ultimately leading to a wave of legislative action in the years that followed.

Significant Legislative Milestones in Payday Loan Regulation

The legislative landscape regarding payday loan bans by state has undergone significant transformations over the years, marked by key milestones that have shaped current regulations. One notable example is the passage of the Consumer Financial Protection Bureau (CFPB) regulations in 2017, which aimed to establish a federal framework for regulating payday lending practices. Although these regulations faced legal challenges and were ultimately rolled back, they underscored the pressing need for consumer protection at both state and federal levels.

States also began to enact their own landmark legislation, with Connecticut implementing a comprehensive ban on payday lending in 2015. This marked a significant victory for consumer advocates and illustrated the growing momentum behind efforts to protect consumers from predatory lending practices. Similarly, Maine instituted stringent regulations on payday loans, including interest rate caps and loan duration limits, setting a benchmark for other states to emulate.

These legislative milestones demonstrate the evolving nature of the conversation surrounding payday lending. As states experimented with different regulatory frameworks, the impacts of these laws became increasingly evident. Research indicated a correlation between stricter regulations and improved financial health among consumers, reinforcing the argument for comprehensive bans or robust regulations.

Moreover, these key milestones have had ripple effects, influencing neighboring states and initiating discussions about the necessity for regional cooperation on payday lending regulations. The ongoing dialogue reflects a growing recognition that effective consumer protection requires not only state-level action but also a coordinated effort to address the challenges posed by the payday lending industry.

Recent Trends and Developments in Payday Loan Legislation

In recent years, the conversation surrounding payday loan bans by state has continued to evolve, mirroring the complexities of consumer credit and financial regulation. States have witnessed an increase in legislative activity, with some opting to strengthen existing bans while others have reevaluated their positions on payday lending. This dynamic environment showcases the ongoing debates regarding the role of payday loans in providing access to credit versus the necessity for consumer protection.

As public awareness of the dangers associated with payday lending has grown, so too has the pressure on legislators to take meaningful action. Recent developments in states like California and New York have seen successful campaigns aimed at implementing stricter regulations, including interest rate caps and mandatory disclosures. These efforts have been bolstered by grassroots advocacy, with consumers and organizations rallying for change and challenging the payday lending industry.

Conversely, some states have witnessed attempts to roll back existing regulations, often driven by lobbying efforts from payday lending organizations. In these situations, advocates have mobilized to present counterarguments, emphasizing the damaging effects of high-interest loans on borrowers. This ongoing tug-of-war between consumer advocates and the payday lending industry highlights the complexities of crafting regulations that effectively address consumer needs while maintaining access to credit.

Overall, the recent developments in payday loan regulation illustrate a broader societal reckoning with issues of financial inequity and the necessity for sustainable lending practices. As states navigate these challenges, the evolution of payday loan bans by state remains a critical focal point for policymakers, consumers, and advocacy groups alike.

Understanding the Impact of Federal Legislation on State Regulations

The relationship between federal legislation and state-level regulations concerning payday loan bans by state reveals the complexities of financial oversight. Notably, the enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act in 2010 significantly impacted the regulatory landscape for payday lending. This landmark legislation aimed to address the underlying causes of the financial crisis and established the Consumer Financial Protection Bureau (CFPB), tasked with overseeing financial products and safeguarding consumers.

The creation of the CFPB marked a turning point in the fight against predatory lending practices, empowering federal regulators to curb abusive lending practices and enforce consumer protections. The Bureau’s proposed regulations sought to impose stricter standards on payday lending, including requirements for lenders to assess borrowers’ ability to repay loans. Although these regulations faced challenges and were rolled back in subsequent administrations, they underscored the necessity for robust oversight to protect consumers.

States have responded to federal legislation in various ways, with some viewing the CFPB’s efforts as a catalyst for implementing their own bans or regulations on payday lending. For instance, states such as Massachusetts and Washington have drawn inspiration from federal initiatives when formulating their regulations, creating a patchwork of laws that reflect both state priorities and federal guidelines. This interplay illustrates how federal actions can serve as a blueprint for state-level reforms, inspiring legislative changes aimed at consumer protection.

However, the ramifications of federal legislation also underscore the ongoing challenges faced by states in regulating the payday lending industry. With online lenders operating across state lines, enforcing state-level bans becomes increasingly complicated. The potential for regulatory arbitrage—where lenders exploit loopholes in state laws to operate in more permissive environments—poses significant challenges for effective oversight. As states grapple with these complexities, the relationship between federal and state regulations continues to evolve, shaping the future of payday loan bans by state.

A Comprehensive State-by-State Analysis of Payday Loan Regulations

A detailed examination of state-by-state approaches to payday loan regulation reveals a diverse landscape shaped by varying legislative philosophies and consumer needs. States such as Nevada and Michigan have adopted more lenient regulations, allowing payday lenders to operate with minimal restrictions. In these states, the payday loan industry remains robust, catering to consumers seeking quick access to cash, albeit at steep interest rates.

Conversely, states like New York and California have implemented stringent regulations or outright bans on payday lending, prioritizing consumer protection over the availability of short-term credit. These legislative differences highlight the varied perspectives on how to balance access to credit with consumer welfare. States with complete bans often cite the negative financial consequences of payday loans, advocating for alternatives that do not expose consumers to predatory lending.

Additionally, some states have introduced innovative approaches to consumer lending, experimenting with community lending programs and credit unions designed to provide accessible, low-interest loans. These initiatives reflect a broader movement toward rethinking the role of financial institutions in serving underbanked populations, championing responsible lending practices that prioritize consumer health and financial stability.

As policymakers continue to debate the merits and drawbacks of payday lending, the state-by-state analysis of payday loan bans by state serves as a critical lens through which to examine the evolving regulatory landscape. This analysis reveals the challenges and opportunities inherent in crafting effective legislation that promotes financial stability while ensuring access to necessary credit.

Evaluating the Impact of Payday Loan Bans on Consumers

The consequences of payday loan bans by state on consumers extend far beyond mere access to credit. These bans can transform financial landscapes, influence consumer behavior, and ultimately affect the overall economic health of communities. Exploring the multifaceted impacts of payday loan bans reveals both the benefits and potential drawbacks inherent in such legislation.

Access to Credit in the Context of Payday Loan Bans

While bans on payday loans are intended to protect consumers from predatory lending practices, they can inadvertently restrict access to quick credit for individuals facing urgent financial needs. For many, payday loans represent a crucial lifeline during crises, providing immediate funds for unexpected expenses such as medical bills or car repairs. When states enforce complete bans, it raises significant questions about the alternative options available for those in need of swift financial solutions.

In states with complete bans, individuals may find themselves compelled to explore less conventional avenues for credit, which can come with their own set of risks. Some consumers may resort to informal lending from friends and family, which can strain relationships and create financial uncertainty. Others might turn to credit cards or personal loans, which, while potentially safer than payday loans, can still lead to debt accumulation if not managed judiciously.

Proponents of payday loan bans stress the importance of establishing robust alternative financial services that cater to consumers’ needs without exposing them to exploitative practices. In states where payday lending is prohibited, community banks and credit unions frequently emerge as essential resources, offering affordable loans and financial education to help consumers navigate their financial choices. By enhancing access to responsible financial products, states can alleviate the adverse effects of payday loan bans on credit accessibility.

Ultimately, the challenge lies in achieving a balance between consumer protection and access to credit. While bans aim to shield consumers from high-interest loans, careful consideration of the broader financial ecosystem is vital to ensure individuals have viable alternatives when seeking quick cash.

Assessing Financial Health in the Wake of Payday Loan Bans

Research indicates that payday loan bans by state can lead to significant enhancements in overall financial health for consumers. Studies have shown that states with stringent regulations or complete bans on payday lending often experience a decrease in reliance on high-cost borrowing. By eliminating payday loans as an option, consumers may be motivated to seek more sustainable financial solutions.

For instance, a study conducted by the Center for Responsible Lending found that states with payday loan restrictions observed a noticeable decline in consumer debt levels. As individuals turn away from high-interest loans, they often become more skillful at managing their finances, exploring alternative credit options, and building savings. This shift can lead to greater financial stability and resilience, as consumers are less likely to become ensnared in the cycles of debt that payday loans frequently perpetuate.

Moreover, the impact of payday loan bans extends beyond individual consumers to the broader community. When consumers are not burdened by payday debt, they may have more disposable income to spend on essential needs, thereby stimulating local economies. This positive ripple effect underscores the interconnectedness of financial health and community well-being, further bolstering the argument for legislative action against payday lending.

However, it is crucial to recognize that the transition away from payday loans may not be seamless for all consumers. Some individuals might initially struggle to adapt to the absence of these short-term loans, particularly if they have relied on them for immediate financial relief. Thus, it is imperative for states to invest in financial education and support services to assist consumers in navigating the changing landscape and developing healthier financial habits.

Exploring Alternative Financial Services in the Absence of Payday Loans

In states that have enacted payday loan bans, consumers frequently turn to alternative financial services to meet their short-term credit needs. While these alternatives can provide necessary access to funds, the quality and cost of these services can vary significantly, raising concerns about their effectiveness in replacing payday loans.

Community banks and credit unions are often viewed as favorable options, offering personal loans with lower interest rates and more manageable repayment terms. These institutions typically prioritize consumer welfare, emphasizing responsible lending practices that contribute to the financial health of their members. Additionally, many credit unions provide financial education resources, empowering consumers to make informed decisions regarding borrowing and budgeting.

However, challenges persist in ensuring widespread access to these alternative financial services. In certain regions, particularly rural or underserved communities, options may be limited, forcing consumers to rely on more exploitative avenues. This dynamic raises critical questions about financial inclusion and highlights the necessity for comprehensive solutions that prioritize access to affordable credit for all individuals.

Furthermore, the rise of technology has introduced new players into the alternative finance landscape, with online lenders offering personal loans and peer-to-peer lending platforms emerging as viable options. While these services can provide quick access to funds, consumers must exercise caution and thoroughly assess the terms and fees associated with these loans. The lack of regulation in some online lending markets can expose borrowers to predatory practices, underscoring the importance of consumer education and awareness.

As states navigate the complexities of payday loan bans by state, ensuring that consumers have access to responsible alternative financial services will be paramount. Policymakers must consider the broader implications of regulatory changes and work toward establishing a financial ecosystem that empowers consumers to thrive.

Examining the Economic Effects of Payday Loan Bans

The economic ramifications of payday loan bans by state extend beyond individual consumers, influencing local economies and shaping broader financial trends. As states grapple with the implications of regulating the payday lending industry, understanding the economic effects of these bans becomes essential for informed policymaking.

Impact on Local Economies and Communities

When states implement complete bans on payday lending, the effects on local economies can be profound. In regions where payday lending has been a significant source of growth and employment, such bans can lead to business closures and job losses. Payday lenders often employ a substantial workforce, and the closure of these establishments can create a ripple effect throughout local economies, impacting not only employees but also ancillary businesses that depend on their patronage.

Moreover, the absence of payday lenders can alter consumer spending patterns. Without access to quick cash, individuals may restrict their spending on necessities and discretionary items, which can lead to a contraction in local markets. Businesses that rely on consumer spending may face downturns, further complicating the economic landscape.

However, the potential for positive outcomes also exists. States with bans or strict regulations often witness a shift toward more sustainable financial practices among consumers. With fewer individuals ensnared in the cycle of payday debt, disposable income may increase, leading to greater spending on essential goods and services. This positive economic effect can invigorate local businesses, fostering a healthier economic environment.

Transitioning from a payday loan-dependent economy to one that emphasizes responsible financial practices requires time and strategic planning. Local governments should consider investing in community resources, financial education initiatives, and alternative lending programs to mitigate short-term economic disruptions caused by payday loan bans.

Business Closures and Relocations in Response to Regulation

The implementation of payday loan bans by state can lead to notable shifts in the operational landscape for payday lenders. In some instances, businesses may choose to close entirely or relocate to states with more lenient regulations. This reaction not only affects the payday lending industry but also has broader consequences for local economies.

In states where payday lending is a significant industry, the loss of these businesses can disrupt employment and tax revenues. Payday lenders often contribute to local economies through job creation and community engagement, and their exit can create a void that is challenging to fill. Regions that once relied on payday lending may need to explore alternative economic development strategies to attract new businesses and stimulate job growth.

Conversely, as payday lenders relocate to more permissive states, competition for consumers can intensify in those areas. This dynamic can lead to increased marketing efforts by payday lenders, potentially luring vulnerable populations in search of immediate financial solutions. The challenge lies in ensuring that consumers in these regions are educated about the risks associated with payday lending and have access to alternative financial services.

As the landscape of payday lending continues to evolve, states must carefully consider the long-term implications of their regulatory decisions. Striking a balance between consumer protection and economic vitality will be crucial to fostering resilient local economies while safeguarding individuals from predatory lending practices.

Broader Economic Implications of Payday Loan Bans

The broader economic implications of payday loan bans by state can reverberate through various sectors, influencing consumer behavior, credit markets, and overall financial stability. As states tighten regulations or impose complete bans, shifts in borrowing patterns can reshape the financial landscape and impact consumer debt levels.

Conversely, research has indicated that payday loan bans can lead to a decrease in overall consumer debt. By eliminating high-interest loans, consumers may be less likely to accumulate unmanageable debt burdens. This positive outcome has potential ramifications for the broader economy, as reduced consumer debt levels can lead to increased spending and investment in local markets.

However, the transition away from payday loans can be challenging for some consumers. The absence of immediate credit options may compel individuals to explore alternative financial products that may carry their own risks, such as high-interest credit cards or loans from less reputable lenders. This underscores the importance of ensuring that consumers have access to safe and affordable borrowing options in the wake of payday loan bans.

Moreover, discussions surrounding payday loan bans often intersect with broader conversations about financial inclusion. As states implement bans, attention must be directed toward ensuring that underserved populations continue to have access to necessary financial services. Fostering the development of responsible alternative lending options will be vital in promoting economic stability and reducing reliance on exploitative financial products.

Ultimately, the broader economic implications of payday loan bans highlight the interconnectedness of consumer finance and local economies. Policymakers must consider these dynamics when crafting regulations to ensure that the outcomes of legislative actions strengthen rather than hinder economic vitality.

Influencing Consumer Debt Levels Through Legislative Actions

The relationship between payday loan bans by state and consumer debt levels is a critical area of study, as legislative actions can significantly influence borrowing behaviors. Research has shown that states implementing bans on payday lending often experience a decline in overall consumer debt levels. By removing high-interest loans as an option, borrowers are less likely to accumulate unmanageable debts.

The cycle of payday borrowing can lead to escalating debt levels, as individuals may take out multiple loans to cover previous debts. Bans on payday loans disrupt this cycle, encouraging consumers to seek alternative financial solutions that are more manageable. Studies have indicated that consumers in states with payday loan bans tend to engage in healthier financial behaviors, such as budgeting and saving, leading to improved financial outcomes over time.

However, it is essential to recognize that the transition away from payday loans can present challenges for some consumers, particularly those accustomed to immediate access to cash. In the absence of payday lending options, individuals may initially experience financial strain as they adapt to new borrowing practices. This highlights the need for comprehensive financial education programs that empower consumers to make informed decisions and develop sustainable financial habits.

Moreover, the impact of payday loan bans on consumer debt levels can have ripple effects on local economies. As individuals experience reduced debt burdens, disposable income may increase, leading to greater spending and investment in local businesses. This positive economic dynamic underscores the interconnectedness of consumer finance and community well-being, reinforcing the case for legislative action against payday lending.

Understanding the nuanced relationship between payday loan bans by state and consumer debt levels is crucial for effective policymaking. By prioritizing consumer protection while fostering access to responsible financial products, states can create healthier financial ecosystems that benefit both individuals and communities.

Addressing Financial Inclusion Challenges Associated with Payday Loan Bans

The issue of payday loan bans by state intersects significantly with the broader conversation about financial inclusion, particularly for underserved populations. While bans aim to protect consumers from predatory lending practices, there is a pressing concern that such regulations could inadvertently limit access to necessary credit for vulnerable individuals.

In states with complete bans on payday lending, consumers may struggle to find alternative financial products that adequately meet their needs. This can be especially true for low-income individuals and those with limited credit histories, who may face barriers to accessing traditional loans or credit cards. As payday loan options disappear, the risk of financial exclusion increases, underscoring the importance of developing alternative solutions that prioritize equitable access to credit.

Advocates for financial inclusion emphasize the need for innovative lending models that cater to underserved communities. Community banks and credit unions are often viewed as valuable resources, offering affordable loans and financial education to help individuals navigate their financial choices. By investing in these institutions, states can promote more inclusive financial ecosystems that empower individuals to make informed decisions about borrowing and saving.

Moreover, the rise of technology has introduced new opportunities for alternative lending solutions, with online platforms and peer-to-peer lending gaining traction. However, it is vital to ensure that these options prioritize consumer protection and ethical lending practices. As the landscape of alternative finance evolves, policymakers must remain vigilant in safeguarding against potential abuses that could arise in the absence of payday lending.

Ultimately, the effects of payday loan bans by state on financial inclusion highlight the complexities of addressing consumer needs within a changing regulatory environment. Striking a balance between protecting vulnerable populations and providing access to necessary financial services will be crucial for fostering equitable financial ecosystems.

Navigating Enforcement and Compliance Issues in Payday Loan Regulations

The enforcement of payday loan bans by state introduces a range of complexities and challenges, as regulators strive to monitor compliance and ensure that consumers are shielded from predatory lending practices. Effective enforcement is critical for the success of any legislative efforts aimed at curbing the payday lending industry and safeguarding individuals from exploitative financial products.

Regulatory Challenges in Enforcing Payday Loan Bans

Enforcing payday loan bans presents significant regulatory challenges, particularly in states where laws are newly enacted or still evolving. Regulators must navigate an intricate landscape of compliance monitoring, as payday lenders may employ various tactics to circumvent prohibitions. For instance, some lenders might exploit loopholes in regulations or reorganize their business models to continue offering high-interest loans under alternative names or structures.

Furthermore, the rapid growth of online lending has compounded the enforcement difficulties faced by state regulators. Online payday lenders often operate across state lines, making it challenging for individual states to effectively monitor compliance. This cross-jurisdictional complexity can lead to situations where consumers remain vulnerable to predatory practices despite existing state bans.

To address these challenges, state regulators must invest in resources and develop comprehensive strategies for monitoring compliance. This may include implementing technology-based solutions to track lending practices, conducting regular audits, and fostering collaboration with federal agencies to share information and best practices. A proactive regulatory approach is essential to ensure that payday loan bans are effectively enforced and that consumers receive the protection they need.

Complications Arising from Online Lending Practices

The rise of online payday lending has introduced significant complications for the enforcement of payday loan bans by state. Many online lenders operate with minimal regulatory oversight, often targeting consumers in states where payday lending is prohibited. This creates a challenging environment for regulators attempting to protect consumers from predatory practices.

Online payday lenders frequently exploit the lack of uniform regulations across states, offering high-interest loans to individuals in states with bans. The prevalence of these practices raises critical questions about the effectiveness of state-level regulations and the need for coordinated efforts to address the challenges posed by online lending.

Additionally, the anonymity of online transactions can make it difficult for regulators to identify and take action against non-compliant lenders. As the online lending landscape continues to evolve, it is crucial for regulators to adapt their strategies and develop robust mechanisms for monitoring compliance in the digital age.

To combat the complications posed by online lending, states may need to consider implementing stricter regulations on online lenders or collaborating with federal agencies to establish a more cohesive regulatory framework. By addressing the challenges associated with online payday lending, states can better protect consumers and ensure the effectiveness of their payday loan bans.

Implementing Consumer Protection Measures in Regulation

States that have enacted payday loan bans by state often implement robust consumer protection measures to ensure compliance and safeguard borrowers. These measures are vital in maintaining the integrity of the bans and protecting consumers from potential abuses.

One such measure includes mandatory disclosures about loan terms, fees, and interest rates, allowing consumers to make informed decisions. Additionally, states may establish complaint resolution processes, enabling consumers to report violations and seek recourse against non-compliant lenders. These mechanisms empower individuals and foster accountability within the lending industry.

Moreover, educational initiatives surrounding financial literacy and responsible borrowing can serve as essential components of consumer protection. By equipping consumers with the knowledge and skills needed to navigate their financial choices, states can enhance the effectiveness of payday loan bans and promote healthier financial behaviors.

Ultimately, the implementation of consumer protection measures is crucial in ensuring that payday loan bans achieve their intended goals. By prioritizing compliance and consumer education, states can create a regulatory environment that promotes financial stability and safeguards individuals from predatory lending practices.

Fostering Interagency Collaboration for Effective Enforcement

Effective enforcement of payday loan bans by state requires collaboration between various state and federal agencies to share resources and strategies. The complexities of payday lending regulation necessitate a coordinated approach that leverages the strengths of multiple agencies to monitor compliance and protect consumers.

Interagency collaboration can take many forms, including information-sharing initiatives, joint investigations, and regulatory harmonization efforts. By working together, agencies can enhance their capacity to address the challenges posed by payday lending and ensure that consumers are adequately protected.

Moreover, collaboration with community organizations and advocacy groups can bolster enforcement efforts by providing insights into the experiences of consumers and identifying areas of concern. Engaging with these stakeholders can facilitate a more comprehensive understanding of the payday lending landscape and inform more effective regulatory strategies.

Ultimately, interagency collaboration is essential for creating a robust enforcement framework that supports payday loan bans by state. By fostering cooperation among various stakeholders, states can ensure that their regulations are effectively implemented and that consumers receive the protections they deserve.

Public Opinion and Advocacy in the Context of Payday Loan Regulations

The dialogue surrounding payday loan bans by state is heavily influenced by public opinion and advocacy efforts. As consumers become more aware of the implications of payday lending, public sentiment plays a pivotal role in shaping legislative action and driving change.

The Role of Consumer Advocacy Groups

Consumer advocacy groups have been instrumental in advocating for payday loan bans by state, emphasizing the detrimental effects of high-interest loans on individuals and communities. Organizations such as the Center for Responsible Lending and Consumer Federation of America tirelessly work to raise awareness about predatory lending practices and advocate for consumer protection.

These groups engage in grassroots campaigns, mobilizing communities to advocate for change and educate consumers about their rights. By organizing events, distributing educational materials, and engaging policymakers, advocacy groups amplify the voices of consumers and drive the conversation surrounding payday lending.

Additionally, lobbying efforts from consumer advocates have resulted in significant legislative victories in various states. Their persistence has led to the enactment of bans and regulations that prioritize consumer welfare, reflecting the power of organized advocacy in shaping policy outcomes.

As public awareness of the dangers of payday lending continues to grow, the influence of consumer advocacy groups will remain a critical factor in ongoing efforts to address this issue.

Understanding Public Support and Opposition to Payday Loan Bans

Public opinion on payday loan bans by state is often divided, with some individuals supporting bans as necessary consumer protections while others argue that such measures limit access to credit. Advocates of bans typically cite the negative consequences of payday loans, emphasizing the need to safeguard vulnerable populations from predatory lending practices.

Conversely, opponents of payday loan bans often highlight the importance of access to credit for individuals facing financial emergencies. They argue that banning payday loans removes a critical lifeline for those in need, potentially leading to increased reliance on more dangerous lending practices or informal borrowing.

This polarized public opinion complicates the legislative landscape surrounding payday lending, creating challenges for policymakers striving to find a balance between consumer protection and access to credit. Engaging with constituents and fostering informed discussions about the implications of payday lending can help bridge the gap between opposing viewpoints and facilitate constructive dialogue.

Furthermore, public opinion can significantly influence the passage and enforcement of payday loan bans. As awareness of the dangers of payday lending grows, lawmakers may be more inclined to take action in response to constituent concerns. Advocacy campaigns that effectively communicate the risks associated with payday loans can help galvanize public support, paving the way for legislative changes.

The Influence of Advocacy on Legislative Outcomes

The interplay between public opinion and advocacy efforts shapes the trajectory of payday loan bans by state, influencing legislative outcomes and regulatory changes. Advocates often mobilize public support through campaigns, petitions, and community engagement initiatives, emphasizing the need for reforms to protect consumers from predatory lending practices.

Legislators who respond to constituent concerns and the voices of advocacy groups can significantly impact the success of payday loan bans. When public sentiment strongly favors action against payday lending, policymakers are more likely to prioritize legislation aimed at curbing abusive practices and safeguarding consumers.

Moreover, the influence of advocacy efforts extends beyond legislative victories. By raising awareness and fostering informed discussions, advocates can contribute to a broader cultural shift regarding payday lending. Changing public perceptions about the acceptability of payday loans can create a conducive environment for further regulatory reforms and encourage policymakers to take a more proactive stance in addressing consumer protection issues.

Ultimately, the influence of public opinion and advocacy on payday loan bans by state underscores the importance of engaging communities and fostering informed dialogue. By amplifying the voices of consumers and advocating for meaningful change, stakeholders can work together to create a more equitable financial landscape.

The Critical Role of Media Coverage and Public Awareness

The media plays a vital role in shaping public opinion and awareness surrounding payday loan bans by state. Journalistic coverage of payday lending practices, consumer experiences, and legislative efforts can bring attention to the dangers associated with high-interest loans and the necessity for regulatory reforms.

Investigative reporting often uncovers the real-life consequences of payday lending, shedding light on the struggles faced by consumers trapped in cycles of debt. By highlighting compelling stories and statistics, media coverage can galvanize public support for advocacy efforts and legislative action.

Moreover, public awareness campaigns can leverage media platforms to disseminate information about the risks of payday lending and the importance of consumer protection. Engaging social media, traditional advertising, and community outreach can amplify messages and educate individuals about their rights and alternatives to payday loans.

As the media continues to cover developments in payday lending regulations, the narratives presented can significantly influence public perceptions and drive advocacy efforts. By fostering informed discussions and raising awareness of the implications of payday loans, media coverage can contribute to a more nuanced understanding of the need for regulatory action.

Ultimately, the role of media in shaping public opinion surrounding payday loan bans by state underscores the importance of awareness and education in driving meaningful change. As consumers become more informed, the potential for advocacy and legislative action increases, paving the way for a more equitable financial landscape.

Grassroots Movements and Community Actions Driving Change

Grassroots movements and community actions serve as powerful forces in advocating for payday loan bans by state. These initiatives often emerge from local organizations and individuals directly affected by the consequences of payday lending, mobilizing communities to push for change.

Grassroots movements typically emphasize the importance of local voices in shaping policy decisions. By organizing events, rallies, and community forums, advocates can raise awareness about the dangers of payday lending and rally support for regulatory reforms. These initiatives create opportunities for individuals to share their stories, fostering a sense of solidarity among those seeking to protect themselves and their neighbors from predatory lending practices.

Moreover, community action can take many forms, ranging from petitions to lobbying efforts aimed at lawmakers. By presenting a united front, grassroots movements can significantly influence public opinion and create pressure on policymakers to prioritize consumer protection. The collective power of communities advocating for change can lead to tangible outcomes, including the passage of payday loan bans and the implementation of stronger regulations.

As grassroots movements continue to grow, they highlight the importance of community engagement in shaping the narrative surrounding payday lending. By amplifying the voices of those most affected by these practices, advocates can work toward a financial landscape that prioritizes consumer welfare and promotes equitable access to credit.

Analyzing Case Studies on Payday Loan Bans

The examination of payday loan bans by state is enriched by specific case studies that illustrate the diverse landscape of legislation and its impacts on consumers and communities. By analyzing both successful and unsuccessful implementations of payday loan regulations, valuable lessons can be learned to inform future policymaking.

California: A Model for Comprehensive Reform in Payday Lending

California serves as a notable case study in the ongoing efforts to effectively regulate payday lending. The state has enacted comprehensive laws that limit the amount of interest payday lenders can charge and impose strict regulations on loan terms. These efforts have been driven by advocacy groups and a growing recognition of the harmful effects of payday loans on consumers.

The implementation of these regulations has resulted in a significant decrease in payday loan usage among California residents. Studies indicate that consumers are less likely to fall into cycles of debt, with many turning to alternatives such as credit unions for responsible borrowing solutions. This case study exemplifies the potential for comprehensive reform to create a healthier financial environment for consumers.

Moreover, California’s approach highlights the importance of consumer education and outreach initiatives that accompany regulatory changes. By equipping individuals with knowledge about their financial options, the state has empowered residents to make informed decisions and navigate their borrowing needs responsibly.

New York: A Consumer Protection Success Story

New York stands out as a success story in the fight against predatory lending practices, having implemented strict regulations on payday lending. The state has adopted a comprehensive approach that includes interest rate caps, mandatory disclosures, and consumer protections aimed at safeguarding borrowers from abusive practices.

These measures have led to a notable decline in payday loan usage, with many consumers reporting improved financial health. Research indicates that individuals in New York are less likely to rely on high-interest loans, resulting in lower overall debt levels and increased financial stability.

Furthermore, New York’s focus on consumer education and outreach has played a crucial role in the success of its payday loan regulations. Advocacy groups have collaborated with state agencies to provide resources and support to individuals seeking alternatives to payday loans. This holistic approach underscores the importance of combining regulatory measures with education to foster a more sustainable financial landscape.

Texas: The Struggles of Partial Regulation in Payday Lending

Texas serves as a compelling case study in the challenges of partial regulation of payday lending. While the state has implemented some restrictions on payday loans, many consumers continue to face high-interest borrowing options that can lead to financial distress. Critics argue that the existing regulations are insufficient to protect vulnerable populations from predatory lending practices, resulting in ongoing cycles of debt for many borrowers.

Despite these challenges, advocacy efforts in Texas have gained momentum, with grassroots movements pushing for more comprehensive reforms. These efforts highlight the importance of public engagement and advocacy in addressing the issues associated with payday lending, as consumers and organizations work together to amplify their voices and advocate for stronger protections.

The Texas case study illustrates the complexities of regulating an industry that continues to thrive in a less restrictive environment. As policymakers grapple with the nuances of payday lending, Texas serves as a reminder of the need for ongoing advocacy and consumer engagement to drive meaningful change.

Ohio: Lessons Learned from Legislative Reversals in Payday Loan Regulations

Ohio’s experience with payday lending regulations offers critical insights into the challenges of maintaining effective consumer protections. The state once had stringent regulations in place that successfully reduced payday loan usage, but legislative rollbacks ultimately weakened these protections, allowing lenders to operate with minimal oversight.

The consequences of these changes were palpable, with reports of increased defaults and financial distress among borrowers. Advocacy groups mobilized to push back against these rollbacks, highlighting the detrimental effects of weakened regulations on consumers. This case study underscores the importance of vigilance in protecting consumer rights and the need for sustained advocacy efforts to prevent legislative backslides.

Ohio’s experience serves as a cautionary tale, illustrating the fragility of consumer protections in the face of political pressures. As advocates continue to fight for stronger regulations, the lessons learned from Ohio can inform future efforts to create a more equitable financial landscape.

Charting the Path Forward for Payday Loan Regulations

The case studies of California, New York, Texas, and Ohio highlight the diverse landscape of payday loan bans by state and the myriad factors influencing the effectiveness of regulations. As states continue to grapple with the challenges posed by payday lending, the lessons learned from these examples can inform future policymaking and advocacy efforts.

A comprehensive approach that prioritizes consumer protection, education, and collaboration among stakeholders is essential for creating a more equitable financial landscape. By fostering ongoing dialogue and engagement, lawmakers can work toward crafting regulations that empower consumers and promote financial stability.

Ultimately, the path forward requires a commitment to protecting vulnerable populations from predatory lending practices while ensuring access to safe and affordable financial products. As public awareness grows and advocacy efforts gain traction, there is hope for meaningful change in the fight against payday loan exploitation.

Frequently Asked Questions About Payday Loan Bans

Which states currently have banned payday loans?

Several states, including California, New York, and New Jersey, have enacted complete bans on payday lending to protect consumers from high-interest rates and predatory practices.

How do partial bans on payday loans operate?

Partial bans allow payday loans under specific conditions, such as interest rate caps or limits on loan amounts, aiming to mitigate risks while still providing access to credit.

What are the potential disadvantages of payday loan bans?

Bans may limit access to quick credit for individuals facing urgent financial needs, potentially forcing them to seek less regulated or more costly alternatives, which can exacerbate their financial situations.

How has federal legislation influenced state payday loan bans?

Federal laws like the Dodd-Frank Act have emphasized consumer protection, encouraging states to implement stricter regulations or outright bans on payday lending practices to safeguard consumers.

What impact do payday loan bans have on consumer debt levels?

Research suggests that payday loan bans can lead to reduced consumer debt levels, as individuals are less likely to engage in high-cost borrowing and more inclined to seek sustainable financial alternatives.

How do alternative financial services function in place of payday loans?

States with payday loan bans often foster community banks and credit unions, providing low-interest loans and financial education to offer responsible alternatives to payday lending.

What challenges exist in enforcing payday loan bans?

Enforcement challenges include monitoring compliance, addressing violations, and dealing with online payday lenders operating across state lines, complicating the regulatory landscape.

What is the role of consumer advocacy groups in payday loan reform?

Consumer advocacy groups push for legislative changes, raise awareness about predatory lending, and educate the public on their rights and alternatives to payday loans, playing a crucial role in reform efforts.

How does public opinion affect payday loan legislation?

Public support and opposition can significantly influence the passage and enforcement of payday loan bans, shaping the legislative landscape and prompting lawmakers to respond to constituent concerns.

What lessons can be drawn from case studies on payday loan bans?

Case studies illustrate the varying effectiveness of regulations, emphasizing the importance of comprehensive approaches that include consumer education and advocacy efforts to protect against predatory lending.

See also: Finance & Business.

Jacob Harrison is a dynamic author specializing in a broad range of topics for QuickLoanPro. With a keen eye for detail and a passion for making financial concepts accessible, he helps readers navigate the complexities of personal finance, loans, and budgeting. Jacob’s insightful articles aim to empower individuals with the knowledge they need to make informed financial decisions, blending informative content with practical advice. Through his engaging writing style, he strives to connect with audiences, providing them with valuable resources for their financial journeys.

Ah, payday loans—the financial equivalent of deciding to jump out of a burning building into a safety net made of spider webs. It’s fascinating to see how different states are handling this issue, each with their own flavor of consumer protection, kind of like a buffet of financial regulations where some folks pile their plates high while others just nibble hesitantly on the salad.

You’ve hit on an interesting analogy with the spider webs. It really does capture the precarious situation many find themselves in when considering payday loans. The way states approach regulation is a fascinating study in both economics and human behavior. Some states seem to take a very hands-on approach, almost like protective parents, while others let the market dictate terms—a decision that can leave vulnerable people in the lurch.

I really resonate with your exploration of payday loan bans across the states. It’s fascinating—and somewhat troubling—how different states approach consumer protection in such varying ways. The sheer disparity means that individuals in certain areas still face those predatory lending practices, while others are effectively shielded from the heavy burdens of high-interest debts.

Your analysis of payday loan bans across the United States raises crucial points about the different approaches states have taken to consumer protection. It’s interesting to see how states with complete bans are prioritizing the financial well-being of their citizens, especially given the staggering statistics surrounding payday loan debt. For example, a report from the Consumer Financial Protection Bureau highlighted that nearly 80% of payday loan borrowers re-borrow within a month, indicating how these loans can trap individuals in a continuous cycle of debt.

It’s fascinating to see how payday loan regulations vary so significantly across the states. Growing up in a state where payday loans were heavily restricted, I’ve often reflected on how essential these protections are for individuals who might find themselves in a tight financial spot. The whole concept of payday loans can be quite misleading—what seems like a quick solution often turns into a cycle of debt that is hard to escape.