Understanding the Evolution of Payday Lending Regulations in Virginia

Examining the Initial Regulatory Framework

The journey of payday lending in Virginia stems from a crucial need to shield consumers from predatory lending practices that could lead to significant financial hardship. The late 1990s marked the inception of early regulations designed to promote fairness and transparency within the short-term lending market. These foundational regulations laid the groundwork for subsequent restrictions as policymakers became increasingly aware of the potential for abuse associated with high-interest loans. The introduction of these laws was a direct response to the mounting concerns regarding the financial vulnerability experienced by numerous Virginians, particularly those living on tight budgets and reliant on their paychecks to make ends meet.

Virginia took notable strides toward regulating payday lending by mandating that lenders obtain licenses and adhere to stringent guidelines. These initial measures included requirements for clear disclosure of loan terms and conditions, aimed not only at protecting borrowers but also at nurturing a competitive lending environment. As the demand for payday loans escalated in the years that followed, the state’s regulatory framework encountered various challenges, prompting the need for additional measures. The continuous search for a balance between lender profitability and consumer protection would ultimately shape the ongoing evolution of payday lending laws in Virginia.

Understanding the Effects of Federal Legislation on State Regulations

The impact of federal legislation on the landscape of payday lending in Virginia is significant and far-reaching. Federal laws, especially the Truth in Lending Act (TILA) and the Fair Debt Collection Practices Act (FDCPA), have played a pivotal role in shaping the regulatory framework by ensuring lenders practice transparency and fair treatment of borrowers. These federal regulations provide a backdrop against which Virginia’s specific state regulations have been formulated, ensuring compliance with fundamental consumer rights and protections.

Moreover, the introduction of the Dodd-Frank Wall Street Reform and Consumer Protection Act led to the establishment of the Consumer Financial Protection Bureau (CFPB), an entity designed to oversee lending practices nationwide. This federal oversight has prompted state legislatures, including those in Virginia, to tighten regulations on payday loans, enhancing consumer protection. The interaction between state and federal regulations illustrates the intricate dynamics of the payday lending environment, emphasizing ongoing efforts to safeguard consumers while balancing lender interests.

Tracking the Progress of State Law Revisions

Over the years, Virginia’s payday loan laws have undergone substantial revisions in response to shifting economic conditions and evolving consumer needs. Initially, these regulations established a basic framework for oversight; however, as the payday lending market expanded, the complexities surrounding lending practices also increased. The growth of payday lending throughout the 2000s prompted heightened advocacy for more stringent controls to protect vulnerable borrowers.

By 2010, Virginia enacted significant reforms, including the implementation of tougher interest rate caps and limitations on loan terms. These changes were directly motivated by alarming trends indicating that many borrowers were becoming trapped in cycles of debt due to high-interest loans. Legislative efforts shifted toward cultivating a more supportive financial environment for consumers. The evolution of state laws mirrors not only the changing economic landscape but also the growing acknowledgment of payday loans as a vital issue impacting countless Virginians.

Assessing the Impact of Economic Downturns on Lending Policies

Economic recessions have profoundly influenced payday lending policies in Virginia, as these financial downturns often result in an increased reliance on short-term loans for many households. The Great Recession of 2008 starkly highlighted the financial challenges faced by numerous families, driving more individuals toward payday loans as a means of immediate financial relief. In response to the recession, Virginia lawmakers recognized the pressing need for reforms to safeguard consumers from the harmful repercussions of high-interest loans.

As unemployment rates surged and disposable incomes shrank, the state adjusted its lending policies to better meet the urgent financial needs of its residents. This included enhancing consumer protections and expanding access to financial education for borrowers. By acknowledging the direct link between economic instability and the demand for payday loans, Virginia aims to foster a more resilient financial environment for its citizens, prioritizing responsible lending practices and consumer awareness to empower individuals in their financial decisions.

Adapting to Technological Innovations in Lending

The emergence of online lending platforms has dramatically transformed the payday lending landscape in Virginia, introducing both challenges and opportunities for regulators. The convenience offered by digital lending has increased the accessibility of payday loans, yet it has simultaneously raised concerns regarding predatory practices and the need for robust consumer protection measures. Virginia’s regulatory framework has had to evolve to address this technological shift, requiring a reevaluation of existing laws to encompass online lenders operating within the state.

Digital lending platforms often function across state lines, complicating the enforcement of Virginia’s payday loan regulations. In response, state agencies have intensified their efforts to monitor online lenders, ensuring compliance with interest rate caps and other consumer protection standards. The intersection of technology and regulation continues to shape the future of payday lending in Virginia, with policymakers striving to protect consumers while fostering innovation within the financial services sector.

Current Payday Loan Regulations in Virginia

Understanding Interest Rate Caps and Their Purpose

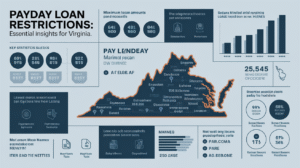

Virginia has instituted specific caps on the interest rates that payday lenders are permitted to charge, aiming to protect borrowers from exorbitant fees that could lead to financial distress. These interest rate caps are a fundamental aspect of the state’s regulatory framework, designed to deter predatory lending practices that can result in overwhelming debt burdens for consumers. Currently, the interest rate cap for payday loans in Virginia is established at 36%, a significant measure intended to ensure that borrowers are not exploited during their financial hardships.

The rationale behind implementing these interest rate caps is based on the understanding that excessive borrowing costs can trap individuals in a cycle of debt that is difficult to escape. By limiting the maximum interest rate, Virginia strives to cultivate a more equitable lending environment where consumers can access short-term credit without being burdened by exorbitant repayment amounts. This regulatory approach reflects a dedicated commitment to consumer welfare, balancing the interests of lenders with the financial security of borrowers.

Despite the existing caps, ongoing discussions persist regarding their effectiveness and appropriateness. Advocates for stricter regulations argue that even a 36% cap is excessively high, particularly for low-income borrowers who may be disproportionately affected. This debate underscores the complexities inherent in payday lending regulations within Virginia, highlighting the necessity for continual evaluation and adaptation of laws to align with the evolving economic landscape and the needs of consumers.

Defining Loan Term Limits to Promote Responsible Borrowing

In addition to interest rate caps, Virginia has established explicit limits on the duration of payday loans, aimed at preventing borrowers from falling into long-term debt traps that can arise from repeated borrowing. Presently, payday loans in Virginia must be repaid within a concise timeframe, typically spanning from two to four weeks. This regulation is crucial in mitigating the risks associated with payday loans, promoting responsible borrowing practices and discouraging the cycle of dependency that can result from prolonged loan terms.

By enforcing strict repayment terms, Virginia encourages borrowers to explore alternative financial solutions rather than relying solely on payday loans. When borrowers are aware that their repayment obligations are limited, they are more likely to seek healthier financial habits and avoid falling into debt spirals. This approach not only benefits consumers but also contributes to a more stable financial ecosystem within the state.

The implementation of loan term limits is further supported by consumer education initiatives designed to inform borrowers about their rights and responsibilities. By fostering awareness around the implications of payday loans, Virginia seeks to empower consumers to make informed financial decisions and navigate their borrowing options judiciously, ultimately reducing the risks associated with excessive borrowing.

Setting Borrower Eligibility Requirements for Protection

Eligibility criteria for obtaining a payday loan in Virginia are carefully outlined to ensure that borrowers meet specific standards before accessing funds. These criteria serve to protect vulnerable consumers from experiencing financial distress by screening for individuals who may lack the capacity to manage the responsibilities associated with payday loans. Generally, to qualify for a payday loan in Virginia, borrowers must be at least 18 years old, possess a valid government-issued identification, and demonstrate a reliable source of income.

By establishing these eligibility requirements, Virginia aims to minimize the likelihood of borrowers defaulting on their loans. Lenders are mandated to conduct thorough assessments of a borrower’s financial situation, which includes income verification and evaluations of debt-to-income ratios. This meticulous process helps to ensure that only those who can reasonably afford to repay the loan are granted access to these funds, thereby enhancing consumer protection.

As the landscape of payday lending continues to evolve, Virginia’s eligibility criteria may also adapt to address emerging trends and challenges. Policymakers remain vigilant in monitoring the market to ensure that regulatory measures effectively protect consumers while allowing responsible lending practices to thrive. Striking the right balance between access to credit and consumer protection remains a focal point in Virginia’s ongoing efforts to regulate payday lending effectively.

Ensuring Compliance and Enforcement of Payday Lending Laws

The Crucial Role of State Regulatory Agencies

State agencies in Virginia play a vital role in enforcing regulations governing payday loans and ensuring that lenders comply with established standards. The Virginia State Corporation Commission (SCC) is primarily responsible for overseeing financial services, including payday lending. This agency is tasked with regulating lender licensing, monitoring compliance with interest rate caps, and enforcing consumer protection laws to safeguard borrowers.

The SCC’s enforcement efforts encompass regular audits and investigations into payday lenders to ensure adherence to state regulations. These proactive measures are essential in preventing predatory lending practices and protecting consumers from exploitation. Additionally, the agency offers guidance and resources for both borrowers and lenders, promoting transparency and accountability within the payday lending market, which ultimately fosters trust among consumers.

Collaboration with other state and federal agencies further enhances enforcement capabilities. By sharing information and resources, Virginia can effectively address concerns surrounding illegal lending practices and bolster consumer protections. The role of state agencies is thus crucial in maintaining the integrity of the payday lending industry and ensuring that borrowers can access fair and responsible financial services.

Consequences for Non-Compliance with Regulations

Lenders in Virginia face substantial penalties for failing to adhere to payday loan regulations, serving as a deterrent against unethical practices. Violations of state laws can result in hefty fines, suspension of licenses, and even criminal charges in severe cases. The consequences of non-compliance are designed to underscore the importance of adhering to established regulations and maintaining ethical lending practices that protect consumers.

For example, lenders who charge interest rates exceeding the legal cap may incur significant fines and risk losing their operational licenses. This strict enforcement framework aims to instill confidence in consumers that they are safeguarded from predatory lending practices. Furthermore, it encourages lenders to adopt responsible business practices that align with the state’s regulatory objectives, supporting a healthier lending environment for all involved.

The penalties for non-compliance represent a critical mechanism for upholding the integrity of the payday lending sector in Virginia. By holding lenders accountable for their actions, the state fosters a more transparent and equitable lending landscape for consumers, reinforcing the commitment to consumer protection and responsible lending practices.

Facilitating Consumer Complaints and Accountability

Virginia has established several mechanisms for consumers to file complaints against payday lenders, thereby aiding enforcement efforts and ensuring accountability within the industry. These complaint channels are crucial for empowering borrowers to express their concerns and seek resolution. The Virginia State Corporation Commission (SCC) maintains an online complaint form that enables consumers to report issues ranging from deceptive practices to violations of lending laws.

Once a complaint is submitted, the SCC undertakes an investigation into the allegations and takes appropriate action to address any identified wrongdoing. This process not only assists in rectifying individual grievances but also contributes to broader regulatory oversight. By analyzing complaint data, the SCC can detect trends and patterns that inform future regulatory adjustments and enforcement strategies aimed at improving consumer protection.

Moreover, consumer advocacy organizations in Virginia play a crucial role in supporting individuals through the complaint process. These organizations provide resources, education, and assistance to consumers seeking to navigate the complexities surrounding payday lending. By facilitating access to complaint mechanisms, Virginia aims to foster a more just and responsive lending environment, reinforcing the belief that consumer voices matter in shaping the landscape of payday lending regulations.

Evaluating the Impact of Payday Lending on Consumers

Access to Financial Resources and Its Implications

The restrictions placed on payday lending in Virginia significantly influence consumers’ access to short-term credit. While these regulations are intended to protect borrowers from predatory lending practices, they may also restrict the options available to those in urgent need of financial assistance. For many Virginians, payday loans represent a quick solution for unforeseen expenses; thus, limitations can pose challenges when access to capital is constrained.

The delicate balance between consumer protection and access to credit presents a complex issue. Stricter regulations may deter some lenders from operating within the state, potentially diminishing immediate funding options for consumers who rely on these services. As Virginia’s regulatory framework evolves, it is essential for lawmakers to consider the implications of access to credit, particularly for low-income individuals who may lack alternative financing avenues.

Consumer education initiatives are crucial in addressing these concerns. By equipping individuals with knowledge about financial management, budgeting techniques, and alternative lending options, Virginia strives to empower consumers to navigate their financial circumstances more effectively. Ultimately, the objective is to ensure that restrictions on payday loans do not inadvertently create barriers to access for those genuinely in need of financial assistance.

Strategies for Preventing Debt Cycles among Borrowers

The restrictions imposed on payday loans in Virginia are primarily aimed at preventing consumers from falling into a detrimental cycle of debt. High-interest rates and short repayment terms can create a perilous loop where borrowers continuously take out new loans to settle existing debts. This phenomenon, often referred to as the “debt trap,” can lead to significant financial instability and distress for numerous individuals.

By enforcing interest rate caps and limiting loan terms, Virginia seeks to disrupt this cycle and encourage responsible borrowing behavior. These regulations motivate borrowers to consider alternative financial solutions rather than relying solely on payday loans, fostering a more sustainable approach to managing financial challenges. The emphasis on preventing debt cycles aligns with broader initiatives to promote financial literacy among consumers, equipping them with essential tools to effectively manage their finances.

Furthermore, Virginia’s approach to debt cycle prevention includes collaboration with community organizations and financial education programs. These initiatives work to raise awareness about the risks associated with payday loans and provide guidance on healthier financial alternatives. By addressing the underlying causes of financial instability, Virginia is taking proactive measures to protect consumers from the adverse effects of payday lending practices.

Enhancing Consumer Financial Education Initiatives

Virginia actively promotes financial education as a crucial element of its strategy to empower consumers regarding payday loans. Recognizing that many borrowers may lack the financial literacy necessary to make informed decisions, the state has implemented various initiatives aimed at enhancing consumer knowledge. These initiatives focus on educating individuals about the implications of payday loans, effective budgeting strategies, and available alternative financing options.

Community workshops, online resources, and partnerships with local organizations play a vital role in delivering financial education to Virginians. By providing accessible information, Virginia aims to equip consumers with the skills needed to navigate their financial situations with confidence. This education is particularly important for individuals vulnerable to predatory lending practices, as it fosters awareness and empowers them to seek healthier financial solutions.

The state’s commitment to financial education reflects a holistic approach to addressing the challenges associated with payday lending. By encouraging informed decision-making, Virginia seeks to reduce reliance on payday loans and promote responsible financial behaviors among its residents. These initiatives contribute to a more financially literate population, better prepared to face the complexities of modern financial systems and make sound financial choices.

Analyzing the Economic Effects of Payday Lending Regulations

Assessing the Impact on Local Economic Health

The restrictions placed on payday loans in Virginia have significant economic ramifications for local communities and businesses. While these regulations aim to protect consumers from predatory lending practices, they also influence the availability of credit within the community. Local economies often rely on a diverse range of financing options, and limitations on payday loans can alter the financial landscape for residents seeking immediate funds.

Small businesses that cater to underserved populations may find that their customer base is affected by the restrictions on payday lending. When consumers have limited access to short-term credit, they may be less inclined to make discretionary purchases, which can adversely affect the revenue of local businesses. Conversely, the increased focus on consumer protection may foster a more financially stable community, ultimately benefiting local economies in the long run and promoting sustainable economic growth.

The relationship between payday loan restrictions and local economies underscores the necessity for a balanced approach in crafting regulations. Policymakers must consider how these restrictions shape financial behavior and access to credit, acknowledging the broader implications for community economic health. Future discussions should concentrate on fostering a supportive financial environment that meets the needs of both consumers and local businesses, ensuring mutual growth and prosperity.

Understanding the Effects on Payday Lenders

Payday lenders in Virginia are navigating operational changes due to the regulatory framework established by the state. The restrictions on interest rates, loan amounts, and term limits require lenders to adapt their business models to ensure compliance while remaining profitable. As a result, many lenders have had to reassess their strategies, placing greater emphasis on customer service, transparency, and responsible lending practices to build trust with consumers.

The competitive landscape has also evolved, with some lenders opting to exit the market in response to stringent regulations. This consolidation may create service gaps, particularly in underserved areas where payday loans are often sought. However, the remaining lenders who adhere to the regulations may benefit from increased consumer trust and loyalty, as borrowers appreciate transparent practices and fair treatment from responsible lenders.

The evolving regulatory framework also encourages lenders to explore innovative approaches to lending. Some have begun incorporating financial education components into their services, helping consumers understand the implications of their borrowing decisions. By aligning with the state’s consumer protection goals, lenders can enhance their reputation and foster positive relationships within the communities they serve, contributing to a healthier financial ecosystem.

Exploring the Influence on Broader Credit Markets

The regulatory framework surrounding payday loans in Virginia extends beyond individual lenders and significantly impacts the broader credit market. By imposing strict regulations, Virginia’s approach influences lending practices and consumer behavior throughout the financial landscape. The focus on consumer protection and responsible lending has prompted lenders to reconsider their strategies, leading to a shift toward more sustainable lending models that prioritize borrower welfare.

As payday loan regulations tighten, borrowers may increasingly seek alternative sources of credit, such as credit unions or community banks, which typically offer more favorable terms. This shift can expand financing options within the credit market, providing consumers with a broader range of choices that align with their financial needs. Additionally, the emphasis on financial education and debt cycle prevention can encourage borrowers to prioritize long-term financial health over short-term solutions, contributing to improved financial literacy and stability.

The interplay between payday lending restrictions and the broader credit market highlights the importance of a cohesive regulatory approach. Policymakers must remain vigilant in monitoring the effects of regulations on lending practices, ensuring that the credit market remains accessible and equitable for all consumers. A balanced approach can stimulate competition, promote responsible lending, and ultimately contribute to a healthier financial ecosystem, benefiting both borrowers and lenders alike.

Public and Political Engagement with Payday Lending Issues

Consumer Advocacy and Its Role in Regulatory Change

Consumer advocacy groups in Virginia actively campaign for more stringent payday loan regulations, motivated by a commitment to protecting borrowers from predatory lending practices. These organizations tirelessly work to raise awareness about the risks associated with payday loans and advocate for policies that prioritize consumer welfare. Their efforts encompass grassroots campaigns, public education initiatives, and collaboration with lawmakers to promote comprehensive legislative reforms aimed at enhancing consumer protections.

A primary objective of consumer advocacy efforts is to highlight the experiences of individuals who have fallen victim to the debt cycle perpetuated by high-interest payday loans. By sharing personal stories and presenting data-driven insights, advocates seek to illustrate the urgency of the issue and galvanize public support for reform. This grassroots momentum plays a pivotal role in shaping the political discourse surrounding payday lending in Virginia, encouraging lawmakers to take action in the best interest of consumers.

Additionally, these organizations often provide resources and support to individuals grappling with financial challenges. By empowering consumers with knowledge and tools, advocacy groups contribute to a culture of informed decision-making, thereby reducing reliance on payday loans. Their dedicated efforts underscore the vital role of advocacy in driving positive change within Virginia’s regulatory landscape, creating a more equitable lending environment for all.

Navigating the Legislative Landscape: Ongoing Debates

Virginia’s legislative bodies engage in continuous debates surrounding payday loan laws, reflecting diverse perspectives on regulation and consumer protection. Lawmakers grapple with the delicate balance between fostering a competitive lending environment and ensuring that consumers are not subjected to exploitative practices. These debates often feature impassioned arguments from both sides, with advocates for stricter regulations emphasizing the critical need for consumer protection, while opponents argue for the importance of maintaining access to credit for those in need.

The discussions regarding payday lending regulations in Virginia are multifaceted, encompassing a range of economic, ethical, and social considerations. Each legislative session brings opportunities for lawmakers to propose amendments, refine existing regulations, and address emerging challenges within the lending landscape. The dynamic nature of these debates highlights the complexity of the issue and the necessity for ongoing dialogue among stakeholders, ensuring that all voices are heard in shaping the future of payday lending.

Public sentiment often plays a significant role in influencing the legislative process, with consumers expressing their concerns and experiences related to payday lending. Lawmakers must remain attuned to the opinions of their constituents, as the demand for consumer protection grows alongside increasing awareness of the risks associated with payday loans. This interplay between public opinion and legislative action is crucial in guiding the future of payday lending regulations in Virginia.

Insights from Public Opinion Surveys on Payday Lending

Surveys conducted in Virginia serve to gauge public opinion regarding payday loan restrictions, offering valuable insights into consumer attitudes and informing policy decisions. These surveys frequently reveal a strong desire among residents for increased protections against predatory lending practices. As awareness of the risks associated with payday loans continues to grow, public support for stricter regulations has become increasingly pronounced.

The findings from these surveys act as a barometer of public sentiment, significantly influencing lawmakers’ decisions concerning payday lending policies. When a substantial portion of the population expresses concern about the impact of payday loans on their financial well-being, it becomes imperative for legislators to consider these perspectives in their deliberations. The responsiveness of policymakers to public opinion fosters trust and collaboration between constituents and their representatives, ultimately enhancing the democratic process.

Additionally, public opinion surveys often highlight a pressing need for increased financial education initiatives. Many respondents express a desire for resources that can aid them in navigating their financial decisions more effectively. By addressing these concerns, Virginia can cultivate a more informed public, ultimately leading to healthier financial behaviors and a reduced reliance on payday loans among its residents.

Future Directions for Payday Lending Regulations in Virginia

Exploring Potential Regulatory Revisions

The future of payday lending regulations in Virginia is likely to be shaped by ongoing discussions surrounding consumer protection and access to credit. As the landscape continues to evolve, potential regulatory changes could further impact both the industry and consumers alike. Lawmakers may consider options such as lowering interest rate caps, extending loan term limits, or introducing new consumer protections to address emerging trends and challenges faced by borrowers.

The dialogue surrounding these potential changes will likely remain informed by public opinion and advocacy efforts. Consumer demands for more stringent regulations are expected to persist, prompting lawmakers to explore policies that prioritize borrower welfare while avoiding excessive restrictions on access to credit. The balancing act between regulation and accessibility continues to be a critical focus for policymakers as they navigate the future of payday lending in Virginia.

Technological advancements are also poised to significantly shape regulatory changes. As digital lending platforms continue to gain traction, regulators may find it necessary to adapt existing laws to encompass the unique practices associated with online lending. This adaptation will require a keen awareness of emerging trends and a proactive approach to consumer protection, ensuring that regulations remain relevant and effective in a rapidly evolving financial landscape.

Understanding the Role of Technology in Shaping Lending Practices

Technological innovations are set to transform payday lending in Virginia, introducing new platforms and methods for loan processing and consumer engagement. As online lending experiences substantial growth, borrowers can access funds more conveniently than ever. However, this increased accessibility presents both opportunities and challenges for regulators aiming to protect consumers from potential abuses within the digital lending space.

The rise of fintech companies specializing in payday loans introduces a new dimension to the lending landscape. These platforms often leverage technology to streamline the application process, making it quicker and easier for consumers to secure loans. While this efficiency can benefit borrowers, it also raises concerns about transparency and the potential for predatory practices that could harm consumers.

Regulators must remain vigilant in monitoring the impact of technological advancements on payday lending. This may involve revisiting existing regulations to ensure they adequately address the unique challenges posed by online lending platforms. By proactively adapting to the evolving technological landscape, Virginia can cultivate a lending environment that prioritizes consumer protection while embracing innovation and the benefits it brings to both borrowers and lenders.

Fostering Community and Stakeholder Collaboration in Regulation

The future of payday lending in Virginia will depend significantly on ongoing community and stakeholder engagement. Policymakers, advocates, lenders, and consumers must collaborate to identify solutions that address the complexities of the lending landscape. Open dialogues can facilitate a deeper understanding of diverse perspectives and inform regulatory approaches that balance consumer protection with access to credit.

Community involvement is essential in shaping policies that truly reflect the needs of Virginians. By actively engaging with stakeholders, lawmakers can gain insights into the challenges faced by consumers and the potential impacts of proposed regulations. This collaborative approach fosters informed decision-making and cultivates a sense of shared responsibility in creating a fair and equitable lending environment that benefits all parties involved.

The future of payday lending in Virginia is not predetermined; it will be shaped by collective efforts to address challenges, seize opportunities, and prioritize the well-being of consumers. Through ongoing engagement and dialogue, Virginia can develop policies that promote responsible lending practices while safeguarding the financial health of its residents.

Frequently Asked Questions about Payday Lending in Virginia

What are the current interest rate caps for payday loans in Virginia?

The current interest rate cap for payday loans in Virginia is set at 36%, aimed at protecting borrowers from excessive fees and predatory practices that could lead to financial distress.

How long do borrowers have to repay payday loans in Virginia?

Payday loans in Virginia must typically be repaid within a period ranging from two to four weeks, depending on the terms established by the lender and the specifics of the loan agreement.

What are the eligibility criteria for obtaining a payday loan in Virginia?

To qualify for a payday loan in Virginia, borrowers must be at least 18 years old, possess a valid government-issued ID, and demonstrate a reliable source of income to ensure they can meet repayment obligations.

How does Virginia enforce payday loan regulations?

Virginia’s payday loan regulations are enforced by the State Corporation Commission (SCC), which monitors compliance, conducts audits, and investigates consumer complaints against lenders to uphold consumer protections.

What penalties do lenders face for non-compliance with payday loan regulations?

Lenders that fail to comply with payday loan regulations in Virginia may face substantial fines, suspension of their licenses, and potential criminal charges for severe violations that undermine consumer protection.

How can consumers file complaints against payday lenders in Virginia?

Consumers can file complaints against payday lenders in Virginia through the Virginia State Corporation Commission’s online complaint form, which allows for reporting various issues related to deceptive practices and lending violations.

What initiatives are in place to promote financial education in Virginia?

Virginia promotes financial education through community workshops, online resources, and partnerships with local organizations to equip consumers with knowledge about budgeting, responsible borrowing, and alternative financial options.

How do payday loan restrictions affect local economies in Virginia?

Payday loan restrictions can significantly impact local economies by influencing consumer purchasing behavior and affecting the revenue of small businesses that rely on discretionary spending by residents seeking short-term credit.

What role do consumer advocacy groups play in Virginia’s payday lending landscape?

Consumer advocacy groups in Virginia work diligently to raise awareness about the risks associated with payday loans, campaign for stricter regulations, and provide essential resources to help individuals navigate their financial challenges effectively.

What is the future outlook for payday lending regulations in Virginia?

The future of payday lending regulations in Virginia may involve potential changes aimed at enhancing consumer protection while addressing access to credit, influenced by public opinion, advocacy efforts, and technological advancements in the lending landscape.

See also: Finance & Business.

Megan Hannford is an insightful author at QuickLoanPro, where she explores a diverse array of general topics related to finance, personal development, and lifestyle. With a passion for empowering readers through accessible information, she distills complex concepts into engaging content that resonates with a wide audience. Megan holds a degree in Communications and brings her expertise in writing and research to create valuable resources that guide individuals toward informed financial decisions.

It’s interesting to see how Virginia’s regulatory framework for payday lending has evolved, particularly given the broader issues of financial literacy and consumer protection. I remember when I first learned about payday loans—it really opened my eyes to how easily people can fall into debt traps when they’re caught in a tight financial spot.

It’s interesting to see how Virginia has navigated the complexities of payday lending over the years. The early regulations indeed reflect a growing awareness of how vulnerable some communities can be to predatory practices. I think it’s crucial for states to recognize that while payday loans can seem like a quick fix in tight situations, they often lead to a cycle of debt that’s hard to escape.

While I appreciate the efforts to regulate payday lending in Virginia, I can’t help but wonder if the measures go far enough to truly address the underlying issues. The licensing and guidelines are certainly steps in the right direction, but they may inadvertently maintain a system that still exploits those living paycheck to paycheck. With the advent of technology, fintech companies have emerged with even more innovative—and often predatory—lending practices that slip through regulatory cracks.

Your discussion on the early regulations of payday lending in Virginia raises important points about consumer protection and financial literacy. While it’s commendable that regulations were introduced to combat predatory lending, I can’t help but wonder whether these measures have truly addressed the underlying issues faced by borrowers, such as the lack of accessible financial education or sustainable income options. For instance, many individuals still find themselves trapped in cycles of debt due to the recurring reliance on high-interest loans.

It’s fascinating to see how Virginia’s approach to payday lending has evolved over the years. The state’s early recognition of the need for regulation was certainly ahead of its time, as many consumers were vulnerable to the cycle of high-interest debt. I appreciate how you highlight the importance of these foundations for fairness and transparency—principles that should be at the core of any lending practice.

The evolution of payday lending regulations in Virginia is indeed a vital topic, highlighting the delicate balance between providing access to credit and protecting consumers from predatory practices. It’s interesting to reflect on how the initial regulatory framework of the late 1990s has had lasting implications, especially considering the financial struggles many face today.

Your analysis of the evolution of payday lending regulations in Virginia highlights a critical issue that has profound implications not only for individuals but also for the broader economic landscape. The historical perspective you present is essential in understanding how regulatory measures emerged as a protective response to consumer vulnerability, particularly among low-income households that often find themselves entangled in cycles of debt due to predatory lending practices.

You’ve touched on a really important aspect of this issue. The relationship between payday lending regulations and consumer protection really is a vital discussion, especially when you consider the impact on low-income households. Many people don’t fully grasp just how quickly someone can fall behind when faced with unexpected expenses.

It’s intriguing to see how the evolution of payday lending regulations in Virginia reflects a broader conversation about consumer protection and financial literacy. Your post highlights an essential aspect of our economy that often gets overlooked, particularly regarding the vulnerable populations who rely on these quick loans.

You brought up a really important point about the evolution of payday lending regulations in Virginia and how it connects to consumer protection and financial literacy. It’s a complex issue, and I think many people often overlook the struggles of those who turn to payday loans in times of need. The financial literacy aspect is particularly critical. Many individuals simply aren’t taught about managing finances effectively or understanding the long-term implications of high-interest loans.

Your analysis of the evolution of payday lending regulations in Virginia highlights a critical aspect of consumer protection that often goes unnoticed until individuals find themselves ensnared in a cycle of debt. The late 1990s indeed marked a pivotal time as the state began recognizing the harsh realities faced by those who rely on short-term loans.

Your exploration of the evolution of payday lending regulations in Virginia highlights a critical intersection of consumer protection and financial education. It’s fascinating to consider how the initial regulations, rooted in the late 1990s, were not just a response to predatory lending practices, but also a reflection of broader economic vulnerabilities faced by many families.

The analysis of payday lending regulations in Virginia is particularly relevant in today’s economic climate, where many people find themselves in similar financial positions as those described in your post. The fact that the regulatory journey began in the late 1990s is compelling; it speaks to the ongoing struggle between consumer protection and the often predatory practices of lending institutions.

It’s fascinating to see how the regulatory landscape for payday lending in Virginia has evolved over the years. I remember when I first learned about payday loans—there was a significant lack of transparency, and many people didn’t fully grasp the potential pitfalls. Your mention of the late 1990s regulations really highlights how crucial it is to protect consumers in such a vulnerable situation.