Payday loan statistics show a market shaped by short-term cash gaps, higher usage among younger and lower-income borrowers, and a heavy reliance on loans for essentials. For context on how those numbers connect to policy, see our overview of payday loan caps in the US.

Quick take

The clearest pattern in payday loan data is that borrowers usually turn to these loans for urgent, everyday expenses, not discretionary spending. Usage is concentrated among adults ages 25 to 44, and the risk grows quickly when a loan is rolled over or used to cover a previous loan.

What the data says at a glance

The strongest stats story is not that payday loans are broadly popular; it is that they are used by people facing immediate pressure and limited options. That is why the numbers often cluster around essential spending, short repayment windows, and financial strain rather than one-time convenience borrowing.

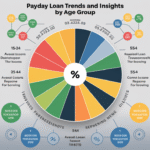

Payday Loan Statistics At A Glance

The national picture is consistent across most data sets: payday loan use is concentrated in households with less financial cushion, and the loan purpose is usually defensive. When borrowers are hit by income volatility, inflation, or a bill they cannot defer, they often use payday lending as a stopgap rather than as a planned financial product. For a broader view of how borrower behavior changes over time, you can also read our payday loan data and trends overview.

Who Uses Payday Loans Most Often

The demographic story behind payday loan statistics is important because it explains the pressure behind the numbers. Most users fall into the 25 to 44 age range, and many are juggling uneven income, rent, transportation costs, childcare, or other recurring bills. That mix of obligations makes the short repayment window especially difficult to manage.

Income is usually the clearest divider. Borrowers with low-to-moderate income often have fewer savings buffers and fewer low-cost borrowing options. They may also face credit barriers that make traditional personal loans harder to get or slower to access. In that environment, payday loans appear fast and simple, even when the overall cost is much higher than the borrower expects.

Employment status matters too. Part-time workers, shift workers, gig workers, and people with unstable schedules are more exposed to timing gaps between expenses and paychecks. That is one reason search demand for payday loans for freelancers and similar flexible-income groups keeps appearing in the broader lending conversation.

Why Age And Income Show Up Together In The Data

Younger working adults are more likely to be in transitional financial stages: first apartments, unstable wages, growing household expenses, or limited emergency savings. When those conditions overlap with low-to-moderate income, payday borrowing becomes more likely because the borrower needs immediate liquidity rather than a long-term credit product.

What Borrowers Use Payday Loans For

Purpose data is one of the most revealing parts of payday loan statistics. About 70% of borrowers use the money for essentials such as rent, utility bills, groceries, transportation, or medical expenses. That matters because it changes the interpretation of the product: this is not mainly spending for convenience, but spending under pressure.

The heavy concentration in necessity spending also helps explain repeat use. If a borrower uses a payday loan to cover an electric bill today, the next paycheck may still not be enough to restore stability. The result is a second loan, a rollover, or another expensive form of short-term credit. From a data perspective, that is where the biggest harm accumulates.

This is also why broader trend pages often overlap with statistics content. A page about payday loan trends among millennials may discuss the same age band, but this article keeps the focus on the actual numbers and what they indicate about borrower need.

What The Economics Of Payday Lending Mean For Borrowers

The economic impact of payday loans is mixed. Lenders can create local jobs, generate revenue, and serve borrowers who might otherwise be shut out of the market. But from the borrower’s side, the data usually points in the opposite direction: high fees, high APRs, and a repayment schedule that can strip away next paycheck flexibility.

That is why the most useful stats are not just about how many people borrow. They are about what happens after the loan is issued. When a borrower must roll over debt or borrow again to cover the first loan, the original problem often gets worse. In practical terms, that means less room for savings, more missed bills, and a greater chance of collection activity.

Signs The Data Points To Financial Strain

- Frequent borrowing to cover basic bills

- Little or no emergency savings

- Rolling over or renewing loans

- Late payments or overdrafts after payday

Why The Cycle Matters

Once a borrower uses a payday loan to make it to the next paycheck, there is often very little margin left to recover. That is why payday loan statistics are often discussed alongside debt stress, financial resilience, and consumer protection.

Regulation And Why State Differences Matter

National statistics are only part of the picture. State rules shape what payday lending looks like in practice, which means the same borrower profile can face very different pricing and repayment terms depending on location. That is why regulation-focused readers should move from this article to the state and cap pages, not the other way around.

If you want the legal side of the market, the better next stop is our page on payday loan restrictions in Virginia. For lawsuits and enforcement history, see payday loan lawsuits. Those pages belong in the regulation cluster; this article stays focused on the numbers.

Need the policy side next?

If you are comparing market data with legal limits, start with the cap-focused guide. It is the clearest companion page for readers who want the rules behind the statistics.

What Payday Loan Statistics Usually Leave Out

Statistics can tell you who borrows, how often they borrow, and what they borrow for. They are less likely to reveal the household context behind the choice. A table can show that many borrowers are ages 25 to 44, but it will not show whether that person is dealing with a car repair, a medical bill, or a temporary reduction in hours. That is why the strongest reading of the data combines numbers with the real-world reasons behind short-term borrowing.

The best use of payday loan statistics is not to sensationalize the product. It is to understand where financial pressure is concentrated and why certain borrowers keep returning to expensive short-term credit. That perspective is more useful for consumers, policy readers, and researchers than a simple yes-or-no judgment about the loan itself.

For readers who want a broader consumer-risk discussion after reviewing the numbers, our page on payday loan pitfalls is the more relevant next step. It expands on the outcomes that the statistics only hint at.

A Few Practical Takeaways From The Numbers

- Payday loan use rises when households face timing gaps between income and expenses.

- The most common borrowers are working-age adults with lower financial cushion.

- Essential expenses dominate, which means the product often fills a basic needs gap.

- Repeat borrowing is the clearest sign that the loan is becoming part of a debt cycle.

- State-level rules can change the cost and availability of the product significantly.

Frequently Asked Questions

What Do Payday Loan Statistics Usually Show?

They usually show that borrowers are concentrated in working-age groups, often have lower incomes, and use the loans for essential expenses rather than optional spending.

Why Do So Many Borrowers Use Payday Loans For Essentials?

Because the loans are often used when a bill cannot wait. Rent, utilities, and medical costs are common reasons borrowers need cash before the next paycheck arrives.

Do Payday Loans Affect Credit Scores?

They can, especially if the loan goes to collections after a missed payment or default. The loan itself may not always be reported, but the consequences often are.

What Page Should I Read If I Want The Rules And Legal Limits?

Start with the payday loan caps guide, then move to state-specific regulation pages if you need local details.

If you are comparing numbers, rules, and borrower risk, the next logical step is to read the regulation pages after this statistics overview. That keeps the data-led intent intact while still giving you the policy context readers usually want next.

Lindsey Moreau is a dedicated author and financial writer at QuickLoanPro, where she explores a range of general topics related to personal finance, lending, and money management. With a passion for making complex financial concepts accessible, she aims to empower readers with the knowledge they need to make informed decisions. Lindsey’s insightful articles are designed to engage and educate, reflecting her commitment to providing valuable resources for individuals seeking financial clarity.

This analysis highlights a crucial issue in the landscape of personal finance. The notable increase in payday loan usage among younger individuals and lower-income groups raises important questions about financial literacy and access to alternative credit options. Many borrowers may turn to payday loans out of necessity, yet the cycle of high-interest debt can be incredibly burdensome.

It’s interesting how payday loans are becoming more prevalent, especially among younger borrowers. I’ve noticed that many people in my circle are turning to these loans for urgent needs like rent or utilities. It really raises questions about financial literacy and access to better alternatives.

I appreciate the depth you’ve brought to the discussion on payday loans. It’s interesting to see how these financial tools are increasingly being utilized by younger and lower-income individuals, as you’ve noted. I’ve seen firsthand in my community how people sometimes feel trapped in a cycle with these loans. It’s alarming to think that a significant portion—about 70%—of borrowers are not using these loans for luxuries but for essential expenses like rent and utilities.

It’s really eye-opening to hear about your experiences in the community regarding payday loans. The statistic you mentioned about 70% of borrowers using these loans for essential expenses like rent and utilities really highlights the desperation many people feel. It raises important discussions about financial literacy and access to more sustainable banking options.

Your insights into payday loan usage trends are deeply thought-provoking and reveal the complex tapestry of financial practices interwoven with socioeconomic factors. It’s important to acknowledge the reality that many individuals are gravitating toward these loans out of sheer necessity. As someone who has witnessed how economic pressures can affect close friends and family, I empathize with the challenging circumstances that spur someone to seek a payday loan, especially when it involves covering essential expenses like rent or utilities.

The trends you outline regarding payday loan usage are indeed concerning and highlight the broader issue of financial vulnerability among lower-income individuals and younger borrowers. It raises an important question about the cycle of dependency created by high-interest loans. For instance, many borrowers might not anticipate the long-term effects of taking out payday loans, often leading to a cycle of borrowing that exacerbates financial distress.

Your analysis of payday loan statistics really brings to light the pressing challenges faced by many in our society today. It’s both troubling and enlightening to see how these loans are primarily used to meet urgent, essential expenses rather than for luxury or discretionary spending. This reality challenges some of the common misconceptions surrounding payday loan borrowers; they are often seen as irresponsible or short-sighted, but your insights highlight that many are simply navigating a system that is not built to support their immediate needs.