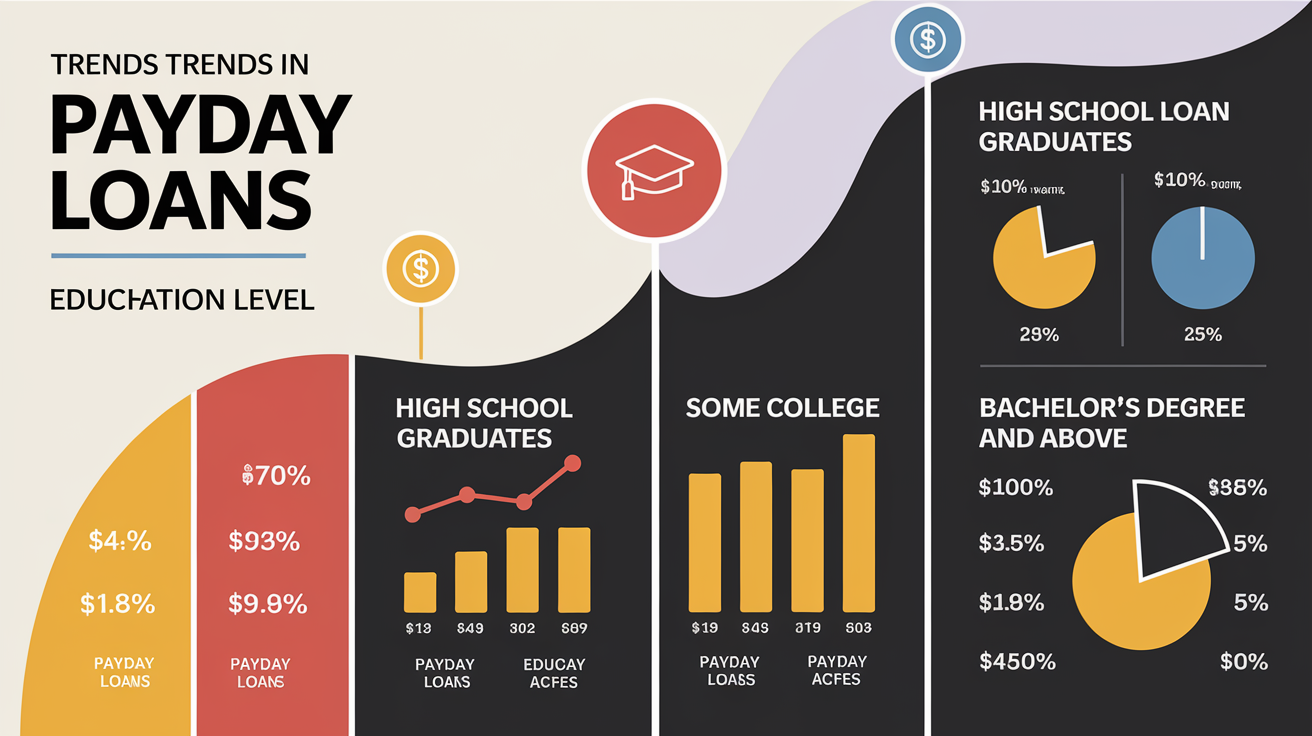

Education Level Is One Of The Clearest Ways To Understand Payday Loan Usage. Borrowing patterns change noticeably from high school graduates to college and postgraduate borrowers, and those differences show up in loan size, repayment stress, and the kinds of emergencies that push people to borrow.

If you want the broader market context too, the cluster page on seasonal demand spikes helps explain when payday borrowing rises, while this article focuses on who borrows by education segment and why.

Education Level Changes The Way Payday Loans Are Used

The short version is simple: borrowers with less formal education tend to use payday loans more often, borrow smaller amounts more repeatedly, and face harder repayment conditions. Higher education does not eliminate payday loan use, but it usually shifts the pattern toward more targeted borrowing, better awareness of alternatives, and slightly stronger repayment outcomes.

That does not mean education alone determines financial behavior. Income, employment stability, student debt, cost of living, and local regulations all matter. But education is still a useful lens because it often tracks with financial literacy, access to credit, and the ability to compare loan terms before signing.

At A Glance

The exact percentages in the source material vary by dataset and graphic, but the directional pattern is consistent: more education generally correlates with lower payday loan dependence and somewhat better repayment outcomes.

What this means in practice

- Borrowers: education can influence how you compare costs, recognize risk, and choose alternatives.

- Lenders and analysts: education is a useful segmentation layer, but it should be read alongside income and employment data.

- Policy readers: the biggest gaps appear when financial literacy is low and local credit options are limited.

If you’re comparing this with other borrower segments, the broader demographics overview shows how education overlaps with age, gender, and household pressure.

High School Graduates: The Highest Exposure To Payday Borrowing

The original content’s strongest case is the high school segment. Individuals with only a high school education make up a large share of payday loan users because they are more likely to face limited wage growth, thinner savings buffers, and fewer fallback credit options. The source material cited a figure near 25% for lifetime use among high school diploma holders, and that fits the broader picture: when an emergency hits, this group often has fewer low-cost choices.

The pressure points are usually familiar. A car repair can threaten a commute, a utility bill can create a cutoff risk, and one missed paycheck can ripple into housing insecurity. In cities with tighter job markets or lower average incomes, such as Detroit and Cleveland, the need for immediate cash becomes more visible. The payday loan is attractive because it is fast, but speed is exactly why the cost can become dangerous.

The source article also noted typical loan amounts in the $300 To $1,000 range. That range matters because it shows how payday loans are usually used for short-term pressure, not large financial planning. Borrowers with a high school education often keep the loan amount relatively small because they are trying to preserve room in an already tight budget. The problem is that small loans are rarely one-off events. One repair, one rent gap, and one bill can become multiple loans within a few weeks.

That repeated borrowing cycle is the real cost driver. A borrower may take $500 to fix a car and then need another $300 for rent before the first loan is gone. Once that pattern begins, the borrower is no longer just managing an emergency; they are managing the rollover risk created by the first emergency.

Why Repayment Is Harder At This Education Level

High-interest pricing is a major issue. The source content referenced APRs as high as 400%, which illustrates how quickly a small loan can become expensive if the borrower cannot repay on the next paycheck. For borrowers with limited savings, even a small fee can be enough to create a chain of missed payments.

The problem is not only the rate itself. It is the mismatch between loan timing and cash flow. Many borrowers in lower-education groups work hourly, shift-based, seasonal, or gig jobs, so repayment may land just when income is least predictable. When that happens, a payday loan can turn into a stopgap for another payday loan.

The source article’s repayment estimate for high school borrowers was also the weakest of the education groups, with about 60% struggling to pay on time. That figure should be read as directional rather than precise across every market, but the takeaway is clear: repayment pressure is materially worse when the borrower has less room in the budget and less confidence about loan terms.

Key risks for this group

- Higher chance of repeat borrowing

- Greater exposure to fees and renewals

- Weaker understanding of APR and total loan cost

- Less access to inexpensive credit alternatives

- Higher stress when income changes week to week

Some College And College Graduates: Lower Usage, But Still Real Financial Strain

College education changes the borrowing profile, but it does not erase the need for short-term credit. The source content indicated that about 15% of college graduates had used payday loans at some point, and that their borrowing is often more situational than habitual. These borrowers are more likely to use a loan for a precise problem: bridge funding between paychecks, tuition shortfalls, moving costs, or a sudden medical bill.

That distinction matters because it helps separate convenience borrowing from chronic dependence. A college graduate might know the loan is expensive and still use it because a rent payment is due before the first paycheck arrives. A new graduate may also be carrying student debt, which shrinks the amount of room available for a temporary cash gap. So while the usage rate is lower than in the high school group, the need can still be very real.

The source material gave a repayment figure of around 45% for on-time payoff among college graduates. That is better than the high school segment, but it still leaves a meaningful share of borrowers vulnerable. The biggest issue is often not lack of intelligence or awareness. It is the transition period: moving into a first job, handling relocation costs, or juggling student debt and monthly living expenses before savings have had time to build.

This is also where financial literacy becomes more visible. College education generally improves the odds that a borrower will compare terms, understand APR, and ask whether a credit union, employer advance, or installment product makes more sense. But the original article correctly notes that higher education does not guarantee better decisions. Stress can overpower knowledge when the bill is due today.

Typical use case

A gap between a new job start date and the first paycheck.

Common pressure point

Student debt or relocation costs that reduce cash reserves.

Decision edge

A clearer ability to compare alternatives, but still a risk of borrowing too quickly.

Postgraduate Borrowers: Less Common, But Often Under Heavier Hidden Pressure

It is easy to assume that a master’s or doctoral degree removes payday loan risk. The source article shows why that assumption fails. Roughly 10% of postgraduates reported using payday loans, which is lower than the other education segments but still notable. In many cases, the borrowing happens during a transition: a move for work, a temporary cash gap, or a period when career earnings have not yet caught up with expenses.

Postgraduates often have stronger financial knowledge, but they can also have higher fixed obligations. Student loans from advanced degrees, professional relocation costs, and social pressure to maintain a certain standard of living can combine into a short-term liquidity problem. The article’s point here is not that postgraduates are careless. It is that advanced education sometimes comes with deeper debt and a more stressful financial runway.

Repayment outcomes in the source material were the strongest for this group, at around 35% successfully paying on time. Even so, that figure leaves room for concern because an educated borrower can still be forced into a poor product when timing is tight. A loan taken to cover a gap after relocating for a new position may look rational on day one and painful two weeks later if the paycheck is delayed again.

This segment is important because it proves the article’s central argument: education lowers the odds of payday loan use, but it does not eliminate financial fragility. The stress may be less visible, but it still exists.

How Education Interacts With Income, Job Type, And Cost Of Living

Education rarely acts alone. A borrower with a college degree but an unstable job can resemble a lower-education borrower in practice if wages are thin and cash flow is unpredictable. Likewise, a borrower with a high school diploma who has steady union work and a manageable housing cost may be less likely to need a payday loan than the averages suggest. That is why the most useful reading of this article is not “more education always equals less borrowing.” It is “more education usually improves the odds, but the surrounding economic environment still drives the decision.”

Employment status is one of the strongest modifiers. Unemployment and underemployment push usage up across all education levels. The original content gave a clear example of a laid-off college graduate turning to payday loans while searching for work. That story is common because timing pressure turns into a credit decision fast. The borrower is not thinking about a year of finance theory; they are thinking about rent, groceries, and utilities this week.

Income level matters just as much. Lower incomes, whether they belong to a high school graduate or a college graduate, increase the odds of payday borrowing because the borrower has fewer built-in buffers. Higher incomes reduce dependence, but they do not remove it if debt obligations are high or unexpected costs arrive at the wrong moment. Student debt, childcare, and medical costs can all narrow the gap between a paycheck and a payday loan.

Cost of living is the last big piece. In expensive cities such as New York City and San Francisco, even educated borrowers can be pushed into short-term borrowing because rent and basic expenses absorb so much income. In lower-cost regions, the pressure may be less intense, but weak local labor markets can cancel that benefit. This is why the same education group can look different across states, cities, and rural areas.

Timing And Seasonality Still Matter

Even though this article is about education, timing still shapes when borrowers use payday loans. The broader seasonal analysis on demand spikes is useful because education-based borrowing often intensifies when seasonal bills, holiday spending, or temporary work slowdowns collide with low cash reserves.

If you are looking at when payday borrowing becomes more likely, the timing question matters almost as much as the demographic question. A college borrower with a temporary relocation cost and a high school borrower facing a holiday utility bill can both end up in the same loan product for very different reasons.

Best Time To Reassess Borrowing

- Before a seasonal income dip hits

- When a job change is about to delay cash flow

- Before rolling one short-term loan into another

- When student debt or rent already consumes most income

- When a lower-cost option is still available

Financial Literacy Is The Real Dividing Line

The most important theme in the original article is not the diploma itself. It is the borrower’s ability to understand cost, compare options, and judge repayment risk. Financial literacy tends to rise with education, but not perfectly. Many college graduates still misunderstand how fees stack up, how quickly short-term borrowing becomes expensive, or how a missed payment affects future options.

That gap explains why some educated borrowers still choose payday loans. They may know the rate is high, but they may not fully internalize the total cost of renewal, the impact of repeated borrowing, or the tradeoff between today’s convenience and next month’s budget stress. The source content correctly argues that education helps, but targeted financial education helps more.

For that reason, college programs, workplace training, and community outreach can make a practical difference. The goal is not to shame borrowers. It is to make the loan decision more visible before it becomes a repayment crisis. Readers who want broader context on repayment management can also compare the advice in payday loan repayment tips, which covers ways to reduce damage after borrowing has already happened.

This is also where the article’s segment-based framing matters. A broad payday loan trends page can mention education, age, rural pressure, and seasonality together, but this page should stay focused on education because that is the cleanest user intent and the safest way to avoid cannibalizing adjacent trend pages.

Regulation And Access Shape The Education Gap

Another reason education matters is that it interacts with the legal environment. State rules can cap interest, limit loan terms, or restrict rollover practices, and those protections change how useful payday loans are in practice. In stricter states, the product may be less available or less damaging, which helps borrowers at every education level. In looser states, the same borrower may be exposed to more expensive terms and fewer safeguards.

The source content pointed to states such as New York as more restrictive and states such as Texas or Ohio as more permissive. That distinction is worth preserving because the educational gap can widen when consumer protections are weak. Borrowers with lower education are often less able to interpret disclosures or spot predatory terms, so the local rulebook directly affects outcomes.

Federal protections matter too, especially through the Consumer Financial Protection Bureau. But rules only help if borrowers know they exist and understand how to use them. A college graduate may be better positioned to recognize a bad loan agreement, while a borrower with less education may sign quickly under pressure. That is why regulation and education should be seen as complements, not substitutes.

For readers comparing legal context across markets, the broader state-law coverage in payday loan laws in 2025 is the right companion article. It explains where the rules are stricter, which helps interpret why education-based borrowing looks different from one region to another.

Where This Leaves Borrowers, Lenders, And Analysts

Education is a useful predictor, but it is not a verdict. A high school borrower may need a payday loan because their only choice is speed. A college graduate may need one because the first paycheck is delayed. A postgraduate borrower may need one because relocation or debt service left no room for an emergency. The common thread is not ignorance alone; it is financial pressure meeting a tight timeline.

For borrowers, the practical lesson is to pause before taking the first available offer. For analysts, the lesson is to treat education as one layer in a bigger model that also includes employment, income, location, and seasonality. And for lenders or market watchers, the education segment is a reminder that access, clarity, and repayment risk do not move in a straight line.

If you are mapping this article against the rest of the site, the adjacent internal pages on age group trends and millennial borrower insights are the most natural next comparisons because they sit beside education in the broader demographics cluster.

A Practical Comparison Of Education-Based Borrowing Behavior

When To Borrow, When To Pause, And When To Look For Another Option

A timing check is useful here because payday loans are often chosen under pressure, not after comparison shopping. If you are a borrower, the best moment to reconsider is before the emergency becomes a rollover. If your next paycheck is already spoken for, the product can be more dangerous than it first appears.

A useful rule of thumb is to pause when the loan would solve one crisis by creating a second one. That is especially important for lower-education borrowers, who may be more likely to use a loan because it is available quickly, not because it is the best value. It also matters for higher-education borrowers who are tempted to assume their degree protects them from bad terms.

When possible, compare the payday loan against an emergency loan, a credit union option, a payment extension, or a short-term budget adjustment. The right choice depends on how quickly you can repay and whether the alternative avoids a rollover cycle.

If You Are Comparing This Page With The Wider Trend Cluster

This article is intentionally narrower than a general payday loan trends piece. That is the right choice because the education angle has a clean search intent and a distinct analytical role. It should support the broader trends cluster, not compete with it.

For a broader lens, the demographics hub is the best next stop. If you want to understand geographic pressure next, the page on rural communities shows how location changes the borrowing story. Together, those pages keep the site’s trend coverage organized by intent instead of repeating the same idea in different wording.

A sensible next step

Use this page when you need the education-specific borrowing story. Use the broader trend pages when you need seasonality, geography, age, or market-wide context.

What The Education Trend Suggests For The Future

The future of payday borrowing by education level will likely keep moving in the same direction unless wage growth, credit access, and financial education improve in tandem. Greater scrutiny of payday lending products may reduce the worst harms, but if the underlying pressure remains — low wages, unstable hours, debt, and high living costs — people at every education level may still reach for quick cash.

That is why the long-term solution is not just regulation. It is also better financial literacy, more affordable credit alternatives, and stronger income stability. When these pieces improve, the education gap in payday borrowing should narrow, especially for the high school and some-college segments that are currently most exposed.

The original article’s strongest insight survives the rewrite: education influences payday loan usage, but it works best as part of a wider economic story. That makes this page a useful supporting node in the broader payday loan trends cluster without competing directly with seasonal or geographic trend pages.

Explore The Wider Payday Loan Trends Context

If you need the broader market lens after reading the education-level analysis, the most relevant next article is the seasonal demand page, which explains when payday borrowing spikes and why those spikes matter.

Frequently Asked Questions

Are Payday Loans Still Popular?

Yes, but their popularity depends heavily on income pressure, state regulation, and the borrower segment being measured. In education-based analysis, the product remains most common among borrowers with less formal education, while educated borrowers still use it when cash flow is tight.

Why Avoid Payday Loans?

The biggest reason is cost. High fees, short repayment windows, and rollover risk can turn a small loan into a long debt problem, especially if your income is unstable or your budget is already stretched.

What Are The 3 C's For A Loan?

The traditional 3 C’s are character, capacity, and capital. In practical terms, that means lenders look at whether you have a record of repayment, enough income to support the loan, and enough savings or assets to handle a setback.

What Is The Biggest Killer Of Credit Scores?

Late payments are one of the most damaging factors, because payment history is a major part of a credit score. Missed payments on any form of debt, including a payday-related obligation that ends up in collections, can cause serious damage.

Which States Banned Payday Loans?

Several states place very strict limits on payday lending or effectively ban the product through rate caps and other rules. Because the legal landscape changes, it is best to check current state-level coverage before assuming a payday loan is available or legal in your area.

Lindsey Moreau is a dedicated author and financial writer at QuickLoanPro, where she explores a range of general topics related to personal finance, lending, and money management. With a passion for making complex financial concepts accessible, she aims to empower readers with the knowledge they need to make informed decisions. Lindsey’s insightful articles are designed to engage and educate, reflecting her commitment to providing valuable resources for individuals seeking financial clarity.

It’s interesting to read about the connection between high school education and payday loan usage, and it really got me thinking about the layers of financial stress many people face today. Growing up, I always understood the importance of getting a degree, but I didn’t fully grasp how significant financial literacy would be in navigating life after school.

It’s really fascinating to hear your perspective on high school education and its connection to financial literacy. You bring up a crucial point about how understanding financial concepts can significantly impact life after school. I remember, for a long time, I thought that just getting good grades and going to college was the key to a secure future. It wasn’t until I started managing my own finances that I realized how steep the learning curve can be.

I came across an insightful piece that dives into the trends shaping payday lending in the coming years, and it really shed light on the ongoing financial challenges many people contend with, especially in relation to their education and financial literacy.

‘Payday Lending Forecast for 2025: What’s on the Horizon?’

https://quickloanpro.com/payday-lending-forecast-for-2025-whats-on-the-horizon/.

This is a really thought-provoking exploration of how high school education intersects with financial challenges, particularly in relation to payday loan usage. It’s disheartening to see that such a substantial percentage of high school graduates find themselves relying on these kinds of loans. It really prompts me to consider the systemic issues at play here.

You’ve hit on something that definitely stirs the pot a bit. High school education and financial challenges—it’s like pairing peanut butter and jelly, where, instead of delicious sandwiches, you end up with a sticky mess that’s hard to digest.

You hit the nail on the head with that one. It’s like watching a circus act where the clowns are juggling textbooks and bills, and the tent is just held up by these payday loans. The fact that so many graduates are leaning on these quick fixes is a real head-scratcher—and it goes way deeper than just bad budgeting.

“I’m glad you found the article thought-provoking! If you’re interested in exploring more about the systemic issues surrounding financial education and alternatives to payday loans, check out this resource.”

https://quickloanpro.com/alexandria-la/payday-loans-grant-parish-la

You’ve hit on a really important issue. It’s tough to see how many high school graduates end up having to turn to payday loans just to get by. It says a lot about not only their financial literacy but broader systemic problems—like the lack of decent jobs for young people or the rising costs of living that outpace wage growth.

I’m glad you found the article thought-provoking! If you’re interested in exploring more about this issue and potential solutions, check out this insightful resource.

https://quickloanpro.com/payday-loans-harvey-la

Your analysis of payday loan usage among high school graduates highlights a critical intersection of education and financial stability. It’s disheartening to think that almost a quarter of individuals with only a high school diploma are compelled to rely on such high-interest loans. This not only raises concerns about financial literacy but also reveals systemic issues in access to supportive resources.

You’ve raised a critical point about the link between high school education and payday loan usage, particularly highlighting the financial challenges faced by graduates in today’s economy. It’s sobering to think that nearly 25% of high school graduates may find themselves relying on such costly financial products. This statistic not only underscores the urgent need for comprehensive financial literacy programs but also invites us to consider the systemic factors that contribute to this reliance.

Your analysis of the link between high school education and payday loan usage highlights a critical issue that often gets overshadowed in discussions about financial literacy. It’s interesting to consider not just the educational aspect, but also the societal structures that contribute to this cycle. For many individuals with only a high school diploma, the job market presents significant barriers, including underemployment and lower wages, which can exacerbate financial vulnerabilities.

You bring up such a crucial point about the interplay between education and economic opportunities. It’s true that for many individuals with only a high school diploma, the job market can feel like an uphill battle. I’ve often thought about how this underemployment, paired with the stress of financial instability, creates a challenging cycle that’s tough to break.

You’ve highlighted a critical issue that often operates beneath the surface of financial discussions. The reliance on payday loans, especially among high school graduates, is a stark indicator of how financial literacy—or the lack thereof—can lead to systemic economic challenges. It’s troubling to think that many individuals are pushed into the cycle of debt without the necessary skills or knowledge to manage their finances effectively.

You’ve really nailed the heart of this issue. It’s eye-opening to see how often payday loans become the go-to solution for folks just starting out, especially recent high school grads who might not have the full toolkit needed for financial management. It makes you think about the bigger picture: we’re not just dealing with isolated personal finance problems here; it’s a signal of a much larger gap in education and support systems.

The insights you’ve shared about the relationship between high school education and payday loan usage truly resonate with me, particularly as they highlight the complexities many individuals face in managing their finances. It’s alarming to consider that nearly 25% of high school graduates find themselves in a position where payday loans become a primary means of addressing financial shortfalls. This statistic doesn’t just illustrate isolated personal choices; rather, it reflects systemic issues that go beyond education, touching upon socioeconomic disparities and the urgent need for broader financial education.

Your analysis of how educational background impacts payday loan usage really sheds light on an often overlooked aspect of financial literacy. It’s striking to consider how many individuals with a high school education find themselves in a position where short-term loans seem to be their only option. Personally, I’ve seen friends and family face similar challenges, particularly when unexpected expenses arise, creating a cycle of debt that can be hard to break.

It’s true, the connection between educational background and payday loan usage often gets overshadowed by more visible issues in financial literacy discussions. Your observations about friends and family resonate with what many experience—those unexpected expenses can throw anyone off balance, regardless of their financial education.

That’s a really important observation; I recently came across some key insights that compare personal loans and lines of credit, which could provide additional context on navigating financial options in tricky situations.

‘Personal Loan vs. Personal Line of Credit: Key Insights’

https://quickloanpro.com/personal-loan-vs-personal-line-of-credit-key-insights/.

You make a solid point about the role of educational background in the conversation around payday loan usage. It’s easy for financial literacy discussions to focus on budget management and investment strategies while overlooking how emotional factors—like the stress of unexpected expenses—can disrupt even the most planned financial paths. That uncertainty can hit hard, regardless of how prepared someone feels.

Your analysis of how education level directly affects payday loan usage is fascinating and deeply relevant, especially in today’s financial landscape. It’s interesting to consider not just the loan size and repayment stress, but also the types of emergencies that push individuals into these borrowing patterns. For instance, high school graduates may face different financial pressures than those with a college degree—often tied to job stability and earning potential.