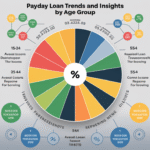

Payday Loan Trends Among Millennials In The Us are shaped less by impulse than by pressure: student debt, uneven income, and the need for fast cash when savings fall short. If you want the broader regulation picture first, start with payday loan caps in the US, then come back here for the millennial-specific view.

The question is not whether payday loans are convenient; it is whether they make sense for a younger borrower trying to manage rent, bills, and credit at the same time.

What Millennials Need To Know First

For many millennials, payday loans fill a gap created by timing, not by long-term borrowing demand. The typical use case is a short emergency: a car repair, a medical bill, a utility shutoff, or rent due before the next paycheck arrives.

That speed is what makes payday loans attractive, but it is also why they can be expensive. Fees and short repayment windows leave little room for error, and the loan can become a repeat expense instead of a one-time fix.

For a broader context on how trend pages connect to behavior, compare this post with our 2025 payday loan data and trends article and the demographics overview.

At A Glance

- Best Fit only for a true short-term emergency with a clear repayment plan.

- Common Risks high fees, repeat borrowing, collections, and cash-flow strain.

- Millennial Pressure Points debt, wage volatility, high living costs, thin savings.

- Better Path compare lower-cost alternatives before you borrow.

Why Millennials Are Using Payday Loans

Student Debt And Thin Margins

Student loans often arrive at the same time as rent, transportation, and everyday bills. That leaves many younger borrowers with little slack when an emergency hits. A payday loan can feel like a bridge, but it is usually a narrow one.

Income Volatility And Gig Work

Millennials are more likely than older groups to rely on freelance work, contract jobs, or uneven schedules. When income changes from week to week, short-term borrowing becomes more tempting because the next paycheck is not always predictable.

High Living Costs

Housing, groceries, insurance, and transportation costs have risen faster than many younger adults expected. Even a small emergency can create a gap that is hard to close without borrowing.

Limited Access To Traditional Credit

Some millennials are still building credit or have credit scores that do not qualify them for lower-cost personal loans. Payday lenders market speed and accessibility, which makes them easier to reach than mainstream options.

What The Costs And Regulations Mean In Practice

The regulatory environment matters because it changes the price and availability of payday loans by state. In stricter states, fees and interest caps can reduce the damage but also limit access. In looser states, borrowers may find more lenders and more aggressive terms.

That is why a millennial borrower in one state may face a very different decision than someone in another. When a loan is available quickly, it still needs to be evaluated on the total cost of repayment, not just the speed of approval.

Why This Matters For Credit Health

Payday lenders may not report a loan the same way card issuers do, but missed payments can still end in collections. For younger borrowers trying to build credit, that can set back future access to car loans, apartments, and mainstream credit products.

If you are already dealing with the fallout, the next step is to look at how to recover after payday loans hurt your credit.

How To Judge A Payday Loan Before You Sign

A quick loan should still pass a basic reality check. If any of these questions produces a weak answer, the loan is probably too expensive for the situation.

- Can you repay it in full on the next payday without missing rent or utilities?

- Do you know the total dollar cost, not just the fee?

- Is there a lower-cost option you can use first?

- Would repeated borrowing make the problem worse next month?

- Have you reviewed your state rules and the lender’s terms carefully?

When A Payday Loan Is Least Risky

The loan is most defensible when the cash need is truly urgent, the amount is small, and repayment is already lined up. Even then, the safest borrower is the one who treats it as a one-time emergency bridge, not a recurring fix.

When To Step Back

If you are already juggling rent, a car note, and other debts, the loan can deepen the strain. In that case, a slower solution like a credit union loan or a hardship plan may protect your budget better.

Digital Borrowing Changed The Trend

Online payday lenders and mobile apps have made borrowing faster and easier for millennials, who are already comfortable managing money on their phones. That convenience can help in a true emergency, but it also lowers the friction that once forced borrowers to slow down and reconsider.

Many platforms now offer instant decisions, 24/7 access, and direct deposit. If you are comparing digital options, also read how online payday loan applications work and what mobile apps change for borrowers.

Security Still Matters

Convenience should never outrun safety. Before sharing bank details or ID information, verify the lender’s legitimacy, review how data is protected, and avoid any offer that pushes urgency over transparency.

For younger borrowers who are especially active online, the security question is part of the decision, not an afterthought.

How Financial Education Changes The Outcome

Financial education does not remove emergencies, but it helps millennials choose better tools when an emergency happens. Borrowers who understand APR, repayment timing, and credit effects are less likely to accept the first fast option they see.

That is why counseling, budgeting basics, and credit coaching matter. They help people recognize a payday loan for what it is: a last-resort bridge that should be replaced, not repeated.

If you are trying to avoid a repeat cycle, the next practical read is payday loan repayment tips, followed by strategies to avoid dependence.

Where The Trend Is Heading

More Digital, More Segmented

The market continues to move online, which means more segmented products, more app-based borrowing, and more marketing aimed at borrowers who want speed over paperwork. That shift helps explain why millennials remain a key audience.

More Pressure For Transparency

As more borrowers compare products online, they are also more likely to notice hidden fees, aggressive terms, and differences in state rules. That makes transparency a central part of the trend story, not just a compliance issue.

Where To Go Next

If you are comparing policy, pricing, and borrower outcomes, the strongest next page is the one that explains the rules in detail. That is why the dominant context for this topic remains payday loan caps in the US.

If your concern is more practical than policy-driven, move to the alternatives and recovery pages that help you choose a lower-cost route or fix the aftermath of a past loan.

Faqs

Are Payday Loans Still Popular?

Yes, but popularity depends on the market, the state, and the borrower group. Millennials remain a visible segment because they often face the exact pressures payday loans are designed to address: immediate cash needs and limited flexibility.

Why Avoid Payday Loans?

The biggest reason is cost. High fees, short repayment windows, and the risk of repeat borrowing can make a small emergency much more expensive than it first appears.

Which States Banned Payday Loans?

Rules vary widely by state, and some states effectively prohibit standard payday lending by capping rates or restricting loan structures. For the details that matter most to borrowers, use a state-specific regulation guide rather than assuming the same rules apply everywhere.

What Is The Biggest Killer Of Credit Scores?

Missed payments and accounts sent to collections are among the most damaging events for credit scores. That is why a payday loan can become a credit issue even when the lender does not report the original loan in the same way as a card issuer.

What Is The 2 2 2 Credit Rule?

People use different versions of this rule, but the common idea is to keep your borrowing habits simple, consistent, and manageable. For millennial borrowers, the practical takeaway is to avoid stacking high-cost debt when a lower-cost option is available.

Megan Hannford is an insightful author at QuickLoanPro, where she explores a diverse array of general topics related to finance, personal development, and lifestyle. With a passion for empowering readers through accessible information, she distills complex concepts into engaging content that resonates with a wide audience. Megan holds a degree in Communications and brings her expertise in writing and research to create valuable resources that guide individuals toward informed financial decisions.

It’s interesting to see the spotlight on payday loans and their impact, particularly on millennials. I resonate with your point about the economic pressures that lead many young people to resort to these high-interest loans. For many of us, balancing student debt alongside rising living costs creates a perfect storm, and the allure of quick cash can be hard to resist.

It’s great to hear that you found the discussion around payday loans and their impact on millennials relatable. The juggle between student debt and climbing living costs can really turn everyday finances into a tightrope walk. It’s a situation many can empathize with.

“Absolutely, the struggle is real for many millennials! If you’re looking for alternatives to manage your finances and avoid the pitfalls of payday loans, check out these resources.”

https://quickloanpro.com/payday-loans-slidell-la

I totally get where you’re coming from. Balancing student debt with rising living costs can feel overwhelming. It’s not just a financial tightrope; it’s like trying to walk a high wire while juggling fire without a safety net. Many of us know that struggle firsthand, and it’s crucial to keep finding ways to navigate it.

“Absolutely! If you’re seeking practical solutions to navigate these financial challenges, I highly recommend exploring this resource that offers alternatives to payday loans.”

https://quickloanpro.com/payday-loans-laplace-la

Payday loans certainly occupy a controversial position in the financial landscape, particularly for millennials navigating significant economic hurdles. As you mentioned, these loans often seem like a quick fix to immediate financial problems, yet they can trap borrowers in a cycle of debt due to their high-interest rates and short repayment terms.

It’s interesting to see how payday loans have become a go-to for so many millennials, especially with the rising cost of living and student debt weighing heavily on us. I’ve had friends who turned to these loans in tough spots, but the high interest can make it a slippery slope. I wonder if more people are exploring alternatives like credit unions or even community programs. It feels like we need more awareness about those options, especially since so much of our generation prioritizes financial literacy. What do you think? Are there better resources out there that can help navigate these situations without falling into the payday loan trap?