Holiday spending is one of the clearest seasonal triggers for payday loan demand, especially when cash flow is already tight. If you are comparing seasonal borrowing patterns, start with the broader 2025 payday loan trends page, then use this article to judge whether holiday borrowing makes sense at all.

The strongest seasonal payday loan spikes usually show up in the weeks before major spending periods, especially late November through December, then again around tax season and back-to-school budgeting pressure. The pattern is less about one holiday and more about a gap between expenses and paydays.

That is why this page stays narrowly focused on Holiday Borrowing Patterns rather than broad market trends. For a fuller seasonal demand comparison, you can also review payday loan seasonal demand spikes.

- Use a payday loan only if the expense is urgent and unavoidable.

- Check whether the repayment date lands before your next full paycheck.

- Compare the total fee to lower-cost options before you borrow.

- Avoid rolling one holiday loan into another short-term loan.

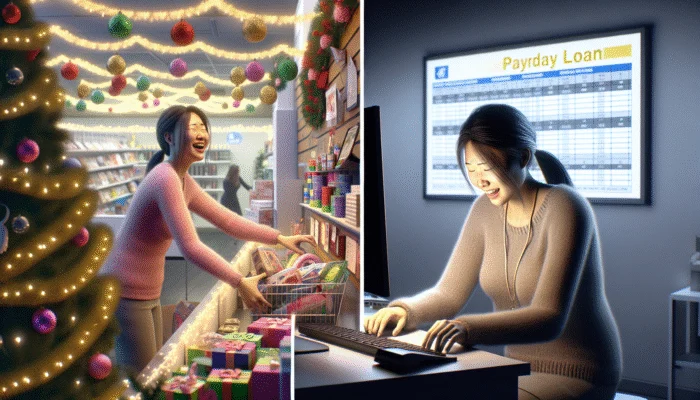

Holiday Demand, In Plain Terms

Holiday borrowing rises when spending spikes faster than income. Gifts, travel, event costs, childcare, shipping charges, and utility bills all compete for the same paycheck, so even people who normally avoid short-term borrowing can feel pushed toward a fast-cash product. The pressure is strongest when a seasonal job ends early, overtime is reduced, or expenses arrive before a bonus or refund does.

That demand pattern matters because payday loans are designed to be quick, not cheap. If you are still deciding whether a short-term loan is the right move, it helps to compare holiday borrowing with broader seasonal options such as holiday budget planning and other lower-cost choices.

Why Holiday Borrowing Gets Expensive Fast

The problem with holiday borrowing is not just the loan itself. It is the way the loan interacts with a season already packed with recurring costs. If a borrower uses a payday loan to cover gifts or travel, the repayment may arrive after the holiday spending is finished but before household cash flow has recovered. That mismatch can create a second round of stress in January.

The original article’s strongest ideas still matter here: repayment strain, credit concerns, and the need for alternatives. But to avoid overlapping with broader market pages, this rewrite keeps those points attached to holiday timing instead of general payday lending trends. If you want a wider context for borrowing behavior, the 2025 data page remains the better broad overview.

The practical question is simple: will the loan be repaid comfortably on the next check, or will it force another short-term fix? If the answer is uncertain, the holiday season is usually the wrong time to borrow.

A Better Order Of Operations

- List the holiday expense and mark whether it is urgent or discretionary.

- Estimate the full repayment amount, not just the borrowed cash.

- Compare the loan cost to a credit card, installment loan, or payment plan.

- Choose the option that fits the next paycheck without forcing another loan.

If your decision is still between short-term products, start with credit cards versus payday loans so you can compare speed, cost, and repayment flexibility.

When To Borrow, When To Wait

| Late October To Mid-November | Start planning if holiday costs are coming. This is the best time to build a buffer, negotiate bills, or choose a lower-cost loan before pressure peaks. |

| Late November To December | Demand is highest and decisions get rushed. If you borrow now, compare total repayment terms carefully and avoid stacking debt. |

| January | This is when holiday borrowing often becomes visible in the budget. Focus on repayment, bill prioritization, and eliminating repeat borrowing. |

| Tax Season And Back-To-School | These are separate seasonal pressures that can create similar borrowing behavior. If your timing shifts away from the holidays, compare the specific seasonal page that matches your need. |

How Holiday Loans Affect Repayment And Credit

The original article spent a lot of time on repayment stress and credit score impact. Those topics stay relevant, but they need a tighter seasonal frame. A holiday loan can affect credit health in practice when repayment is missed, rolled over, or paired with other debts. The cost is not only the fee; it is the pressure the loan adds to a budget that is already absorbing seasonal spending.

Borrowers with variable income feel this most sharply. Retail, hospitality, logistics, and event staff may earn more during the holidays, but that income can fall quickly once the season ends. When that happens, the loan deadline can arrive right after the earning window closes. For workers with unstable schedules, a short-term loan can turn into a sequence of extensions or late payments rather than a clean bridge to the next paycheck.

Credit Score Reality

A payday loan may not report the way a conventional installment loan does, but repayment behavior still matters. Missed obligations, debt collections, and repeated borrowing can leave a lasting mark on your financial profile even when the loan itself was meant to be temporary.

Repayment Warning Signs

- You need a second loan to cover the first.

- The due date lands before your next guaranteed paycheck.

- Holiday spending pushed out essentials like rent or utilities.

- You have no margin for a late fee, overdraft, or emergency expense.

Lower-Cost Alternatives Worth Checking First

The original post correctly pointed to alternatives, and that section is one of the most useful parts of the piece. In a seasonal rewrite, those options deserve a clearer place in the decision flow. If the holiday expense is real but not immediate, or if your paycheck can handle a slightly slower solution, a lower-cost choice often preserves far more flexibility than a payday loan.

Start with the option that best fits the expense type. For smaller or flexible costs, a payment plan may solve the problem without borrowing. For short-term cash needs, compare a credit union loan or emergency loan before committing to a high-fee product. If your household income is stretched by design, consider the broader alternatives guide at effective solutions for low-income borrowers.

Alternatives That Usually Deserve A Look Before A Holiday Payday Loan

- Credit Union Loans often lower cost and easier to manage than a payday loan.

- Employer Advances useful if the shortfall is temporary and your employer offers one.

- Payment Plans good for utilities, medical bills, repairs, and some retailers.

- Credit Cards may still be expensive, but usually offer more breathing room than a payday loan.

- Emergency Loans better when you need speed but want a more structured repayment path.

How To Plan Ahead For The Next Holiday Cycle

A seasonal article is only useful if it helps the next decision, not just the current one. The best defense against holiday borrowing pressure is to plan before the season starts. That usually means setting aside even a small amount each month, identifying gift and travel priorities early, and deciding in advance which expenses are non-negotiable and which can be cut if cash gets tight.

If holiday demand is part of a recurring pattern in your household, the right question is not simply whether a payday loan is available. It is whether the budget can be adjusted sooner so that the next peak season does not create the same emergency. For some readers, that may mean using broader budgeting guidance, while for others it may mean reviewing state rules or lender terms before borrowing. The state-by-state page on payday loan laws in 2025 is the right follow-up if legality or limits matter to your decision.

Where To Go Next If You Are Comparing Options

If your goal is to understand the broader market, go to the 2025 trends and data page. If your question is specifically about seasonal spikes, compare this article with the seasonal demand spikes guide. If you are deciding whether to borrow at all, the most useful next read is a direct comparison of short-term alternatives such as credit cards versus payday loans.

If holiday costs are already in front of you, make the decision with the repayment date in mind, not just the approval speed.

Frequently Asked Questions

Megan Hannford is an insightful author at QuickLoanPro, where she explores a diverse array of general topics related to finance, personal development, and lifestyle. With a passion for empowering readers through accessible information, she distills complex concepts into engaging content that resonates with a wide audience. Megan holds a degree in Communications and brings her expertise in writing and research to create valuable resources that guide individuals toward informed financial decisions.

You bring up some really important points about holiday spending and the pressures that come with it. I’ve definitely been in situations where I overshot my budget, especially with gift-giving and festive events. It’s wild how the holidays can create a kind of “spending frenzy” that blurs our financial judgement.

You’ve raised an important point about the timing of payday loan demand around the holidays. It’s fascinating how the pressure of consumer spending can create financial strain, pushing many into short-term borrowing solutions. I’ve seen firsthand how quickly holiday expenses can stack up, especially with gifts, travel, and festivities, leading families to make tough choices.

This really hits home for me. The holiday season can be such a financial tightrope walk, especially when you have a lot of unexpected expenses popping up. I’ve been in a position where I had to make quick financial decisions during the holidays, and it’s never easy. It’s interesting how the demand for payday loans peaks right when people are expected to be celebrating. I guess that gap between when we need to pay for gifts and when those paychecks come in can really create a sense of urgency.